You might be thinking about building your own home but are wondering how does construction financing work?

Today we’ll show you how construction financing works, what documents you will need to arrange a building home loan and how to process progress payments to get your builder paid!

Let’s dive right in…

Table of Contents

What is construction financing?

Buying a finished house and building a property are two completely different things. Construction financing is used for basic renovation, to construct a home from scratch or to do substantial renovations.

It is a specialised lending option for individuals who are renovating or building a house, as it facilitates them in successfully completing the entire construction process.

Construction financing is a home loan with a construction facility where the bank will pay the builder in smaller instalments, called progress payments while building the house.

Why is construction financing complicated?

It is not easy to build a house. In fact, it is a very complex process that involves multiple stakeholders.

The following are the key stakeholders involved in the construction of a home:

- Solicitors

- Contractors

- Builders

- Lenders

- Quantity Surveyor

- Accountants

- The Council

So many parties are involved in the process, which can be quite challenging sometimes.

For example, one expert may not be able to understand the field of the other party, which can lead to errors and complications.

A large number of financial institutions and mortgage brokers are not familiar with construction at all. This can lead to problems such as g approval of incorrect loan amounts and delay in loan disbursement due to constantly changing requirements.

What construction loan documents do I need?

As with a regular home loan, you will need your latest payslips, a few months’ savings statements and other supporting documents—but you will need a few extra things to get a construction home loan. These are:

- Building Contract. The building contract contains things like the construction stages, progress payment schedule, how long the build time is and the price to construct your new home. Here is an example of a full Queensland HIA Building Contract. The good news is that in Queensland, you do not need to sign the building contract to get your finance approved!

- Building Plans. Before your home loan is approved, you do not need council-approved building plans, but building plans will give the valuer an idea of the property layout and size.

- Specifications. The building specifications give the bank, and valuer, an idea of the types of finishes you will be using in the house and the quality of materials for items like benchtops and appliances. This can make a big difference in the final valuation of the property.

- Extra Quotes. Extra quotes can be anything from solar panels to a pool and even additional landscaping. It is worth giving these to the bank’s valuer so they can determine if these will improve the overall property’s value.

How does construction financing Work?

Construction financing is different from a regular home loan. For traditional financing, a person receives a lump sum loan at the settlement date. Whereas in construction financing, a person receives progress payments from the financial institution at various stages of construction.

What are the stages of construction?

There are typically five progress payments at different stages, including:

- Slabs poured

- Frame up

- Completion of brickwork

- Lock up

- Practical completion

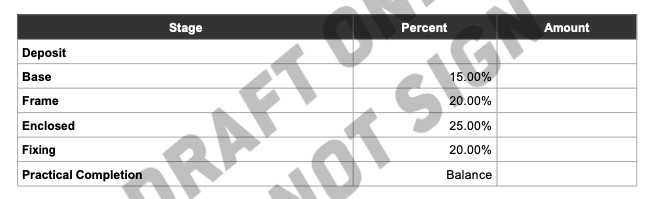

What does a standard HIA progress payment schedule involve?

Banks will often say your builder isn’t following the standard HIA Progress Payment Schedule, which means the builder has changed the amounts you need to pay at the different stages of the construction.

Typically the builders will want to get paid more upfront, but the banks want to spread the payments throughout the construction to spread your risk.

With this being the case, the banks will want you to follow the standard HIA Progress Payment Schedule, which has payments split like this:

- Deposit: 5%

- Base 15%

- Frame 20%

- Enclosed 25%

- Fixing 20%

- Practical Completion 15%

Using an independent valuer

Some financial institutions or banks hire an independent valuer who verifies whether the work has been completed to the standard. The next payment is released only when the valuer provides verification of the work. This can be an effective measure to evaluate the progress of work.

Determining the loan value

In addition to the loan application, banks need a copy of a tender or building contract as well as the construction plans.

The valuer will then assesses what the value of the property will be after completion and also calculates the estimated loan value.

The loan value represents the lower of the two:

- On completion value, or

- Land price plus construction cost

Additional documents required from the builder

Once the builder starts receiving the progress payment after loan approval, he needs to provide the following documents:

- The final plan approved by the council

- Insurance plan

- Drawdown schedule

How does a bank pay the builder directly?

You can ask your bank to send progress payments to the builder. For example, once you receive an invoice from a builder:

- Complete the drawdown request form and sign it.

- The form and invoice are sent to the construction department of your bank.

- The bank may need a valuation to verify the completed work.

- Your lender releases further payment to your builder within five business days.

The same process is repeated at every stage of construction.

Payment mechanism

The progress payments are also called drawdowns. A person is liable to pay interest on the drawdown amount. For example, you get a loan approval for $300,000. However, you only draw $50,000 at the beginning. This means you are only required to pay the interest due on the drawdown amount until you draw an additional amount.

At the construction time, the borrower only pays the interest as loan repayment. This provides comfort by reducing financial burden during a stressful period.

You have 2 options for paying the loan:

- principal and interest, or

- you can continue to keep it as interest only.

Which option you choose depends on the lender and financing option you avail.

Knowing the mechanism of construction financing and how it works is very important. It allows you to prepare a good plan and have all the documents ready, along with a good estimate of the overall cost.

Can all banks do building loans?

While most of the major banks can do building loans and construction finance, not all smaller lenders and online banks can offer it.

This is because these banks view construction finance as very time-consuming and riskier than a regular home loan.

After settlement, the lender needs a team to process progress payments and ensure the builder completes the work.

If the bank is slow at processing progress payments, your builder can get frustrated and delay things. So, you want to work with a bank that is good at the construction process and can make payments quickly.

Right now, in 2024, smaller online lenders like UBank and ING Direct do not allow building and renovation loans.

Speak to home loan experts

If you would like to chat about getting a home loan, we’d be delighted to help you out. Speak with one of our experienced mortgage brokers to walk through the next steps with you.

At Hunter Galloway, we help home buyers get ahead in this competitive market. We give you the actual strategies that have helped other home buyers like you secure a property when there have been 5 other offers on the table! Enquire online or give us a call at 1300 088 065.

Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Start again

Start again