When couples separate in Australia, deciding what to do with a shared home can be challenging. Figuring out how to calculate buying someone out of a house fairly is a common concern.

There are difficult personal choices to make, and the process is further complicated by legal and financial issues.

This comprehensive guide explains the options for buying out your ex’s share of the house, focusing on how to calculate buying someone out of a house in Australia.

We’ll walk you through how to start the process and determine each person’s share of the home’s value equitably.

Whether you’re just beginning to consider your options or are already working on a buyout agreement, this article provides valuable information to help you make informed decisions.

We’ll cover the key steps, including preparing your finances, negotiating the buyout terms, and completing the legal and financial transactions.

To learn more about how to calculate buying someone out of a house in Australia, watch the video below or read on for our detailed guide.

Table of Contents

Quick Summary

- When separating from a partner and deciding what to do with a shared home in Australia, the main options are buyout, sell and split, or keep owning together.

- To buy out your partner’s share, get your finances in order, have the home valued, and learn about mortgage options.

- Negotiate the buyout openly and fairly, with help from mediators and lawyers.

- Calculate the buyout amount by determining the home’s equity (market value minus remaining mortgage) and dividing it according to ownership percentages.

- Consider tax impacts, emotional aspects, and future planning when completing the buyout process.

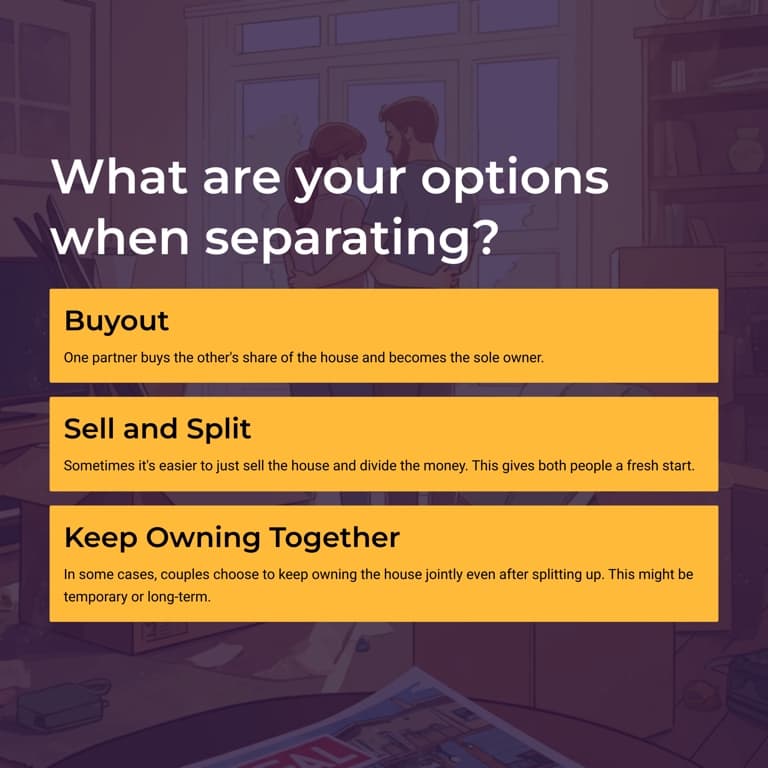

What are your options when separating from a partner?

When couples separate and own a home together, there are usually three main options:

- Buyout: One partner buys the other's share of the house and becomes the sole owner.

- Sell and Split: Sometimes it's easier to just sell the house and divide the money. This gives both people a fresh start.

- Keep Owning Together: In some cases, couples choose to keep owning the house jointly even after splitting up. This might be temporary or long-term.

Choosing the Best Option for You

Deciding what to do with a shared home when separating is a big choice. The three main options – buyout, sell and split, or keep owning together – work better in different situations. Here are some things to think about with each.

Buyout

- Can you afford to pay the other person’s share and handle the mortgage alone?

- Do you want to stay in the home for emotional reasons or to keep things stable for kids? While this is important, be careful you’re not sacrificing too much financially for emotional reasons.

- Does the property work for your long-term plans? Staying could be good if you want to remain in the area.

Sell and Split

- Selling gives both people a clean break financially and emotionally. It splits things simply and fairly.

- Consider if the housing market is good for selling now.

- Think about where you’ll live after selling – will you have enough money to buy or rent a new place?

Keep Owning Together

- Keeping the house could provide consistency for kids. It could be temporary until selling is better. However, this can be messier and more difficult to manage.

- If the market is bad for selling, waiting and co-owning allows more time.

- If you choose this option, make sure you have agreed on a clear plan for selling the home or buying out your partner’s share of the house.

Making Your Decision

There’s no one-size-fits-all option. Get input from lawyers, financial advisors, and real estate agents to understand your full situation. Think about budgets, emotions, and future plans. This is a big choice for your money and wellbeing, so consider carefully!

Steps to Buy Out Your Partner

1. Initial Preparation

If you decide that buying your ex’s share of the home is best, here are some key things to do first:

Get Your Finances in Order

- Talk to a mortgage broker to review your budget and what you can afford.

- Look at your income, expenses, savings, loans, and more. This helps know if you can handle the buyout.

- Discuss options to get money for the buyout, like using savings or getting a loan.

- If you’d like us to review your situation, our Brisbane mortgage brokers can help. Contact us for a free assessment or give us a call on 1300 088 065

Have the Home Valued

- Get an independent certified valuer or agent to formally value your property. This is vital for calculating your ex’s share.

- The valuation considers recent area sales, the home’s condition, market trends, and more. This info helps both the buyout and your future investment.

- Make sure the valuer understands the local market and have valued similar homes before.

Learn About Your Mortgage Options

- If you have a joint mortgage, talk to your lender or a broker about putting the loan under just your name.

- They’ll check if your income, credit, and obligations allow you to qualify for a new loan.

- Explore different products to see what loan terms may suit your new situation best.

After organizing your finances, having the property valued, and researching mortgages, you’ll be in a better position to move ahead with the buyout process.

2. Negotiating the Buyout

After getting your finances straight and having the property valued, the next big step is negotiating the buyout details with your ex. This can be tricky but having some supports in place helps.

Communicate Openly and Fairly

- Have honest talks about what you both want and expect. Listen carefully to understand your ex’s views.

- Any deal absolutely must be fair for both people—consider legal rights and emotional connections.

- Remember this impacts both your futures in big financial and emotional ways.

Get Professional Help

- Mediators facilitate talks, offer neutral advice, and guide you through disagreements.

- Legal advisors make sure deals follow all laws properly and formalise contracts.

- Many couples use both mediation to negotiate and lawyers to finalise agreements.

Set Things Up for Success

- Have all budget information, property valuations, etc. handy for fact-based talks.

- Be ready to compromise some wishes and keep expectations realistic.

- Know that this process can be lengthy and emotional. Respect and patience matter.

Balancing openness, fairness, and professional support can lead to a buyout contract that works for both people—setting you both up for brighter futures.

3. Completing the Buyout

After agreeing on the buyout terms, you need to formalise everything legally and financially:

Transfer Ownership Legally

- Use a conveyancer or lawyer to file paperwork to shift ownership from both names to just yours.

- A conveyancer or property lawyer handles filing the right documents properly.

- They’ll organise a settlement date to finalise legal and money transactions.

Refinance Your Home

- If you have a joint mortgage, you’ll need to refinance in your name only. This releases your ex from the loan.

- The lender decides if you can afford the full mortgage based on your finances.

- Discuss the new loan’s rate, repayment period, and other terms with the lender.

Document Everything

- Draft a contract outlining every buyout detail like amounts and timelines.

- Have your lawyer review to ensure it is binding and protects you.

- Both of you sign the needed paperwork and file it with authorities.

- Keep copies of all documents related to the buyout.

Completing all legal, financial, and paperwork steps ensures you smoothly become the property’s sole owner.

How to Calculate Buying Someone Out of a House

Understand How Home Equity Works

A key piece is deciding how much money your ex gets in the buyout. This depends on the home’s total equity and valuation.

Understanding Home Equity

- Equity means how much of the home you fully own, not counting any mortgage debt.

- To get the equity, first find the property’s current market value. Then subtract what is still owed on the mortgage.

- For example: a $500K home with a $300K mortgage has $200K equity.

How Valuation Impacts Equity

- The market value can shift a lot based on market conditions, nearby sales, the state of repair of the home, and other factors.

- So you need an independent, certified valuer to consider location, size, age, trends, and other things.

- If the valuation increased since purchase, there is likely more equity to split, and more owed for a buyout.

Getting the equity and valuation right is vital for figuring out a fair buyout amount to offer your ex for their share.

We’ll look next at exactly how to calculate this.

Factors that affect the buyout price

The buyout price involves more than basic math. Things like mortgages, home upgrades, and housing markets change the calculations.

Mortgage Amount Left

- The remaining mortgage owed directly lowers the total equity to split.

- Example: A $500K home with a $200K mortgage has $300K equity to divide. One partner’s $150K share is more than if the mortgage was $300K, leaving $200K equity.

- If you refinance the mortgage yourself, the new loan also impacts budgets.

Home Improvements

- Upgrades and renovations can raise the property value, increasing the equity and buyout price.

- Keep paperwork on big home projects to show valuers to justify higher prices.

- But some outdated redos like old kitchens may not boost value much now.

Shifting Housing Markets

- Property values rise and fall a lot based on demand, economy, and many other reasons.

- Current market conditions greatly sway valuation timing—sellers’ markets differ from buyers’ markets.

- Local changes like new construction or businesses affect value too.

Considering every factor that impacts the equity is key to get to a fair buyout amount. This helps make sure your ex gets their fair share.

An example of the buyout calculations

Let’s walk through some sample numbers to understand better how to determine your ex’s share. We’ll also look at special cases.

Basic Calculation Example

- House market value = $600,000

- Remaining mortgage = $250,000

- Total Equity = $600,000 (value) – $250,000 (mortgage) = $350,000

- 50/50 ownership split

- Each share = $350,000 equity / 2 people = $175,000 buyout

Step-by-Step

- Get a professional property valuation

- Check remaining mortgage amount

- Subtract mortgage from property value to determine equity

- Divide equity by ownership share (50/50 here)

- Buyout number is your ex’s share

Unique Situations

- Adjust if ownership percentages differ from 50-50

- Factor in if one person paid more of the mortgage

- Account for home upgrades paid for primarily by one partner

- Consider pending market changes that alter near-future value

These examples provide general guidance. Every situation differs a bit. Consult financial and legal pros to tailor the math for fairness.

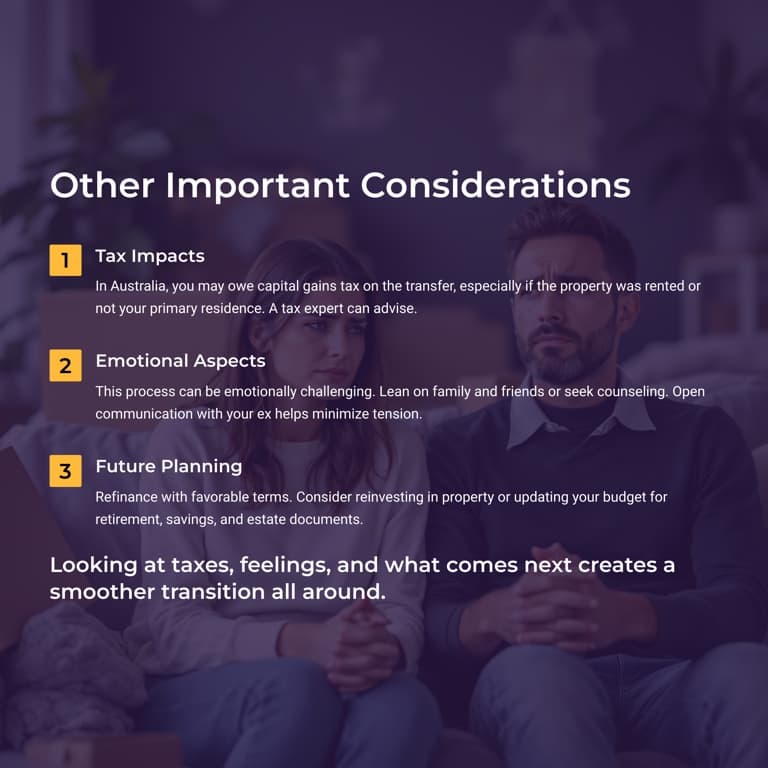

Other Important Considerations

Beyond the money and legal steps, there are a few other key things to think about when buying out an ex.

Tax Impacts

- In Australia, you may owe capital gains tax when transferring property, even between ex-partners.

- There are exemptions if it was your primary home. But if you rented part of it out or didn’t live there full-time, you may owe taxes on part of the gains.

- Investment properties especially can incur taxes based on the difference between original purchase and sale prices.

- A tax expert can explain the laws and what applies to your situation.

Emotional Aspects

- Ending a chapter of shared home ownership can be really tough emotionally.

- Get support from family and friends or see a counselor. Having people to lean on makes a big difference.

- Communicate openly and respectfully with your ex throughout the process to minimize tension.

Future Planning

- If refinancing, get favorable repayment terms that match your money plans.

- Consider reinvesting in property for personal use or as a rental investment.

- Update budgets for retirement, savings goals, etc. to factor in the buyout.

- Change your will and estate documents to show the property’s new status.

Looking at taxes, feelings, and what comes next creates a smoother transition all around.

Pitfalls associated when you are looking at paying out your ex?

Having trouble agreeing on what the property value is.

This is a really common one because if you talk to a real estate agent versus getting a bank valuation, there can be two vastly different valuation outcomes, which can lead to one party thinking the property is worth more or less than what the other thinks.

Real estate agents tend to be more optimistic about the value of a property, while banks tend to be more conservative about the value of the house. Realistically, the value of your home will be somewhere between these two valuations. While it may be difficult to agree on the value of the property, it is not impossible. Just make sure you put your agreement in writing.

Time frames

The other pitfall we see is time frames. You might have agreed on a price a year ago, but it’s taking you a whole year to get your tax returns and things finished, and the market moves. So the house can now be worth more, and you don’t want you or the other person feeling like they are getting less than what the property is worth.

It’s no good if partner A now wants $500,000 instead of the agreed $100,000. In this case, you need to agree on a price (again). You may even want to engage real estate agents to determine how much the property is now worth. In this case, it is best to get a formal commitment saying I agree to transfer this amount. You don’t want to do any handshake deals. Get advice from a solicitor to help you out here and ensure everything’s in writing.

Continuing to pay the mortgage

If you are starting proceedings and going through that separation, but things haven’t been finalized, you need to make sure you’re still paying the mortgage, even if the other party is refusing to pay. This is because having a bad repayment history or credit blemishes will affect your ability to secure finance in the future.

Banks keep a 24-month record of your mortgage and credit card repayments on your credit file. So even if you sold that property but fell behind in repayments, the banks will see that, which can affect you when applying for future mortgages.

Sometimes, lawyers can advise you or your partner to stop making repayments to speed up things, but that will ultimately work against you. If you are having financial hardship, you need to call the bank and have a discussion with them to find out what options they have—such as moving the loan to interest only. Maybe you’re ahead in repayments and can use those extra repayments to stop the repayments. But don’t do anything until you talk to the bank and make sure they won’t put any bad marks on your credit file.

You need to be prepared to apply for a home loan

When buying out your ex, the bank looks at everything as if you’re applying again because you’re all on your own now. You don’t have your partner’s income or situation included, so they’re reassessing the full application.

Therefore, you’ve got to make sure that you’re in a steady income, you’ve got a steady role, your credit’s fine, and obviously, you have equity in the property. The bank will also look at your savings accounts and spending accounts. They’re going to look at your home loan history and many different things that you might not have been expecting because you already have the loan.

So, if you are considering buying out your ex, ensure all your finances are in order.

Frequently Asked Questions

Will I need to pay stamp duty again when I buy out my ex-partner?

In most cases, you won’t need to pay stamp duty again. But generally, you will need court orders, a binding Financial agreement, or something from the solicitor to confirm that this has been done as part of a separation.

We have had clients who go the other way and say they’re happy just to split at 50/50 or say you can sell to me for 500,000, and therefore avoid going through a solicitor. In this case, you may have to pay stamp duty since there are no legal documents or court orders. So keep that in mind. Speak to a solicitor and weigh up the pros and cons. If the stamp is only $500 or $600, it’s probably not going to matter. But if it’s tens of thousands, it’s worth getting a solicitor involved.

Can I just take over the loan and remove my partner from all documents?

The answer to that is no. Unfortunately, the bank will need to reassess it. They see this as a critical change to the loan contract. They’re saying, well, half of the borrowers on the loan are no longer there, so we don’t know if you got the capacity. Therefore, as we said, it’ll go through a full application.

Do I need a separation agreement?

In many circumstances, the bank wants that separation agreement so they know what’s happening with the assets. They also want to be sure that if they refinance this property into your name, they won’t have any issues where the partner comes back to claim it in the future.

The other thing they get from a separation agreement is custody of children. For example, you might have four children, and one of the partners only gets custody 25% of the time. Some banks will take that into consideration and be less harsh when assessing your living expenses. But if there’s maintenance, they’ll take that out of your expenses. So keep that in mind.

What if we get a bad Bank valuation?

The good thing is we have a number of lenders on our panel, so if you get a low valuation from one bank, we can go and get a valuation from another lender, and sometimes that can help. In other cases, if the property is consistently getting valued low by many banks and there’s not enough equity to do the separation, we will let you know. In this case, you may not be able to complete the transaction, and you might need to sell the property and split the assets. Once again, that’s the last resort, and we don’t see much of that. Usually, getting another bank to value the property fixes the issue of low valuation.

Key Takeaways and Next Steps

Splitting up and buying out a shared home involves weighing options around money, legal issues, emotions, and the future.

Main Things to Remember

- Evaluate all alternatives thoughtfully – buyout, sell, or continue owning together.

- Prepare thoroughly – get professional advice, understand legal processes, organize finances.

- Negotiate fairly and legally with mediators and lawyers.

- Calculate the buyout amount considering all factors influencing value.

- Handle emotional, tax, and forward-planning aspects holistically.

Get Professional Support

Because this is complicated, advice from financial, legal, tax, and real estate pros is highly recommended. They can tailor guidance to your situation for the best decisions.

We Can Help

Hunter Galloway offers a free assessment to understand your specific needs and provide expert recommendations. Going through this alone is hard, so let our experienced team help guide you. Call 1300 088 065 or contact us to get started.

With the right information and balanced approach, the property buyout process after separation can have fair and positive outcomes for everyone.

Start again

Start again