This is the most comprehensive guide to using inheritance as a deposit.

In this expert-written guide, you’ll learn everything you need to know, including how to work with banks when buying a house with inheritance and the technical processes and steps required. So if you’ve just been given an inheritance and are unsure where to start, you’ll love this guide.

Let’s dive right in.

Table of Contents

Getting an inheritance & where to go from there

Inheritance is often an unexpected gift for most of our clients.

There is not much information about buying a home with inheritance money because it is a rare and irregular situation. But that is where we come in. In this section, we will go through how inheritance works and what happens from the time you get it.

How does getting an inheritance work?

Let’s start by understanding the jargon around inheritances – mainly the word ‘estate’.

An estate can be defined as—the assets belonging to the person that passed away.

Often the deceased would have previously written a will determining how the estate should be divided. An executor is then appointed to ensure the estate is divided according to what is in the will. However, if there was no will in place, the estate will be divided evenly by the court, which will choose an administrator.

Once the estate has been divided, the remaining debts will be paid out, and then assets will be distributed.

In most cases, how inheritance is paid comes down to the fine print, which influences how the amount is paid, for example, in small instalments instead of a large sum.

There may also be restrictions on what the inheritance is used for — e.g. for education purposes only. Other inheritance terms can include the money being released after certain milestones have been achieved, e.g. university or high school graduation.

Where to go from there?

The time frame of when you will receive your inheritance varies greatly—it can sometimes be a time-consuming and lengthy process.

The positive is that once the money has been released into your account, it is yours to do as you please.

Using an inheritance as a deposit

Inheritance can be used for many things, and using it as a deposit towards buying a home is definitely one of them.

But there are a few factors you need to be aware of before you start making offers on houses.

In particular, there are 2 important factors that most banks want to confirm before giving you a home loan.

- Prove the inheritance payment is non-refundable

To qualify for a home loan using inheritance, the payment must be non-refundable, and you need to be able to prove it. Usually, a letter from the executor confirming the details of the amount and when it was given to you as a beneficiary will do.

In some cases, you’ll also need a copy of the will and Grant of Probate. Ask your solicitor or executor for a copy of this; it shouldn’t be hard to get your hands on it.

- Show the inheritance funds in your bank account.

Once you’ve proven that the money is rightly yours, you’ll need to show the funds in your bank account or in a statement that has the name of the executor or trustee from the deceased estate.

If the inheritance isn’t in your name, you’ll need a letter outlining that you can legally access the funds.

All amounts must be identical to what is in the executor’s letter.

Now, depending on who you are lending with, the timeframe of how long the funds need to be in your account will vary.

How much can I borrow?

You’ll be able to qualify for a home loan if you have at least 5% of the property value available, which can come from the inheritance. Anything lower, and you’ll be at risk of getting your loan declined.

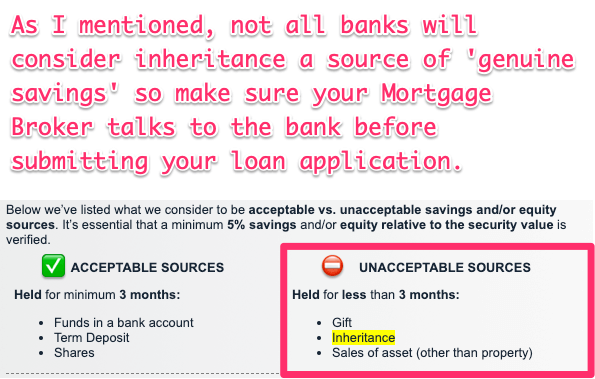

Now, even if you can show your 5% deposit, there is another challenge some banks will present: genuine savings.

What are genuine savings?

Genuine savings are there to show lenders you have a bit of ‘hurt money’ in the property. Most lenders like to see 5% of the property purchase price saved in a bank account for at least 3 months, but this rule has a few exceptions.

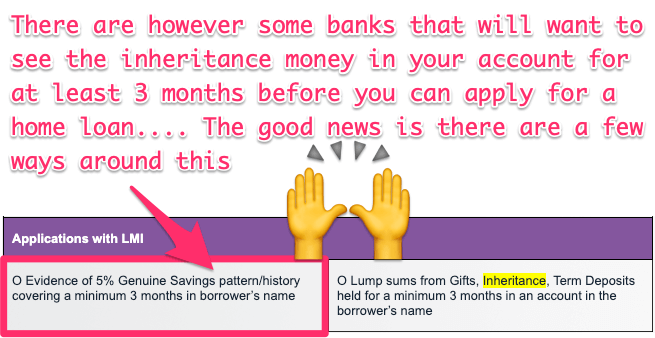

In other words, some lenders will want to see you hold the inheritance in your account for 3 months before being able to buy a home. But the good news is that not all of them want to see the money in your account for 3 months.

You may be able to get around the genuine savings requirement if:

- You have more than a 10% deposit when buying the home.

- You are currently renting and have at least 6 months of clean rental history. This proves you are stable and make regular repayments.

- You look at other banks that don’t require genuine savings.

You can borrow up to 95% of the property value with specific lenders. And the best part is that you’ll be treated the same as a borrower who has saved the deposit themselves.

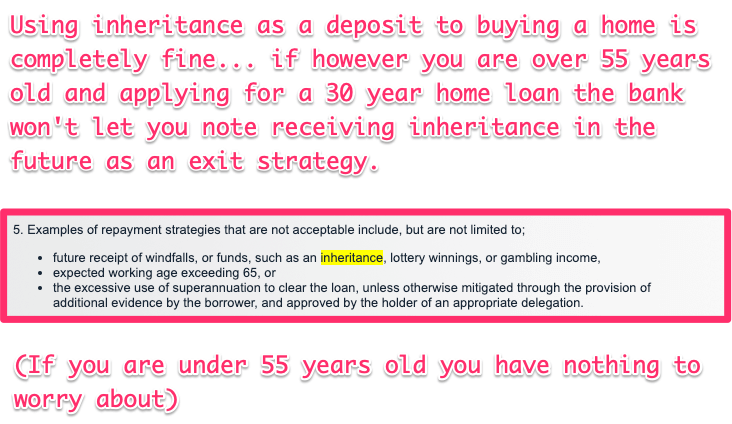

So, in reality, receiving an inheritance will make no difference to the borrowing process— as long as the money is non-refundable.

But if you are borrowing more than 8-% of the loan-to-value ratio (LVR), you will still need to get Lenders Mortgage Insurance. And finally, don’t forget that just because you’ve got a sum of money doesn’t mean that the rest of the lending criteria don’t apply. You’ll still need a good credit history, low debt and enough income to maintain the loan. You’ll be treated as a regular home buyer, with no exceptions.

The ultimate benefit of using inheritance as a deposit is that you’ll be able to speed up the process of getting into the property market.

Am I eligible for the First Home Buyers Grant still?

Good news – If you’re buying a house with inheritance money, you are still eligible for the First Home Owner’s Grant!

The amount of the grant varies between states. However, it can be up to $15,000.This extra boost could help cover the costs of Government fees and solicitor fees.

All the same processes and eligibility requirements remain the same. For example, in Queensland, the grant only applies to new builds, those buying off the plan or structurally renovated properties meeting certain criteria.

Will the bank look at me badly because I haven’t saved the money myself?

When buying a property with an inheritance, you are viewed just like any other borrower. The same interest rates and offers are available for you as a buyer. You will not be penalised or receive any different treatment when buying a property with an inheritance.

So no, the bank won’t look at you badly just because you haven’t saved the money yourself.

The bank will review your income and eligibility as a buyer. As we mentioned above, you need to have good credit and be eligible to take out the loan you are applying for, even if you potentially have a large sum of money to put down as a deposit.

Read More: How Much can I borrow from the banks?

Should I buy a house or pay off personal debt with the inheritance?

Now that you have all the information for buying a property with inheritance money, it’s time to consider other debts.

It can be easy to dream about supercharging what you’ve got right now and buy a new property.

But, if you have pre-existing debt, the question is, should you pay it off first, and which debt should you begin with?

This one will come down to your personal situation, but let’s look at a quick example.

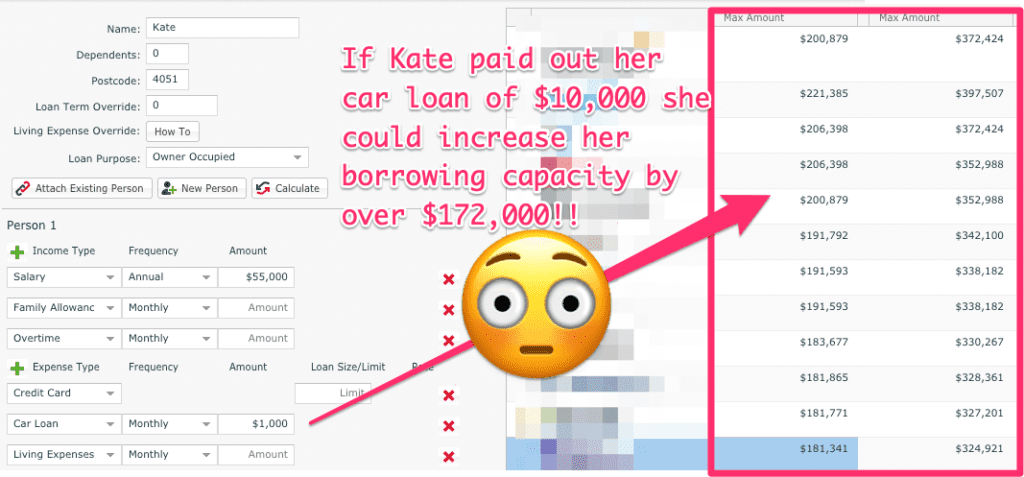

Kate has received an inheritance of $40,000 from her grandmother, who has passed away.

She has a car loan of $10,000 which costs $1,000 per month.

Should Kate pay out the personal loan or leave it open?

(If your personal loan or other debts are going to reduce your borrowing capacity, then it could make sense to pay them off.)

In Kate’s case, her personal loan reduced her borrowing capacity by $172,000, so she decided to pay it out.

Want to see what is best for your situation? Get in touch with our mortgage brokers.

Read More: Maximising your borrowing power.

Next steps and getting your home loan

Have you just received an inheritance and want to buy a house but are unsure what steps to take next?

Our team at Hunter Galloway is here to help you buy a home in Australia. Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please give us a call at 1300 088 065 or book a free assessment online to see how we can help.

Start again

Start again