This is a complete guide to navigating the coronavirus pandemic with a home loan.

In this all-new guide you’ll learn about:

- Impact of COVID-19 on the property market

- Buying during the coronavirus pandemic

- Options for refinancing

- Deferring home loan repayments

- Fixing your home loan

- FAQs

And lots more, so lets get started.

Chapter 1: The Impact of COVID-19 on the property market

Let’s kick things off with an overview of the impact of COVID-19 on the property market.

Specifically, in this chapter I’m going to cover the economic impact of the coronavirus pandemic and what that means for property prices.

Lets dive in.

How has coronavirus affected the economy?

The global coronavirus pandemic is causing economic disruption on a massive scale. This should come as no surprise to you unless you’ve been living under a rock (or you’ve been taking self isolation measures to the next level).

Social distancing, border closures and other measures that our government has taken to control the spread of coronavirus have drastically affected our economy.

Two-thirds of Australian businesses (66 per cent) have reported a drop in their turnover or cashflow due to the coronavirus, according to the Australian Bureau of Statistics.

And it doesn’t stop there – Australian consumer confidence is at an all-time low, the share market is down, and economists are predicting that unemployment in Australia could reach up to 10 per cent.

Thousands of Australians have already lost their jobs, and the federal government estimates that 1 million people could be unemployed as the economic effect of the coronavirus sets in.

Is property in Brisbane going to follow the share market?

We’ve already seen the effect of COVID-19 on our share market. The ASX saw a massive crash from an all-time high of 7,162 on February 20 down 36.5 percent to 4,546 on March 23.

Stock prices have recovered to some degree since then, but there is still massive volatility as the market responds to the latest good (or bad) news about the coronavirus pandemic.

So we know that the share market has taken a beating. But the real question is: are property prices going to go the same way?

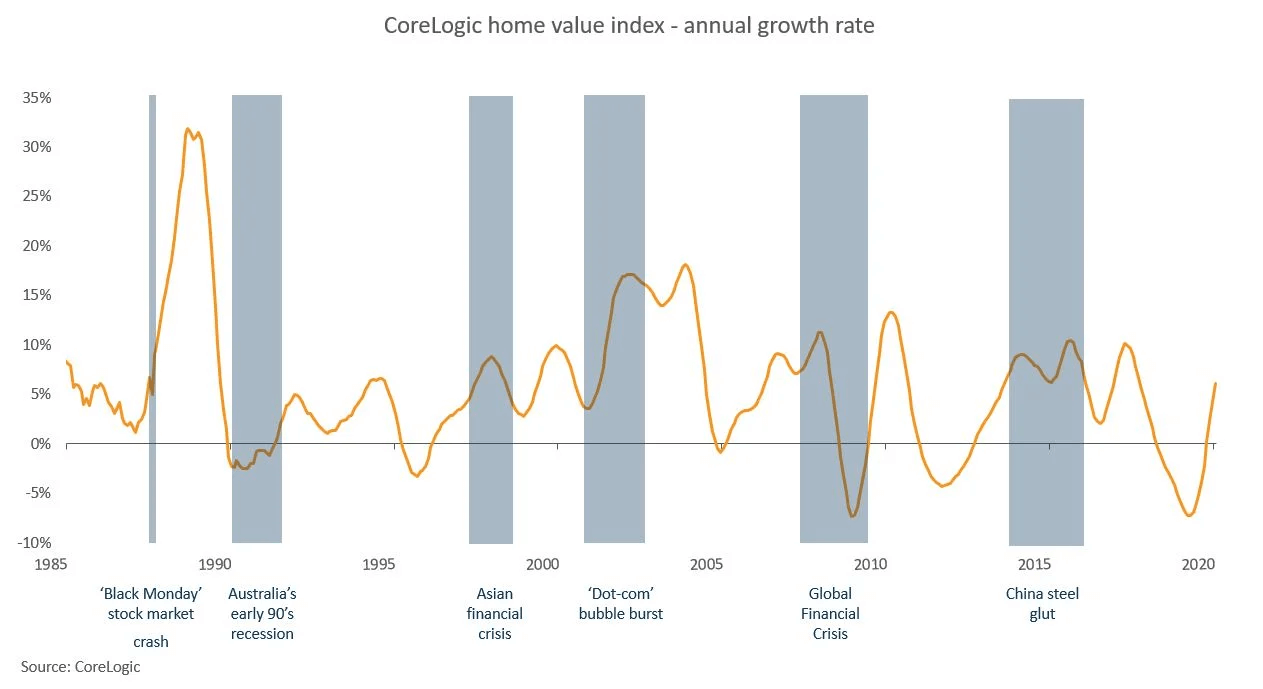

Looking back in history, we can see that residential property has performed relatively well at times of negative economic shocks.

But it’s too soon to know for sure how things are going to go. The share market is forward looking and tends to drop quickly when there is a crisis. The property market usually moves a lot slower, and will often take longer to react to a crisis.

This is because the property market is mostly made up of home buyers, not investors, which makes unemployment the major determining factor of the market.

While the property market has fared well during past economic shocks, we are in unknown territory – there is no clear cut evidence of how it will perform during a pandemic.

Read More: Brisbane Property Market

How has coronavirus impacted the property market to date?

The property market is slower to react to economic changes than the stock market, but we’re already seeing evidence of significant changes in the property market due to the coronavirus pandemic. Here are the main three things we are seeing:

1. Uncertainty is very high at the moment

Consumer confidence and job security are major purchasing decisions when people are considering buying a home. And in the current environment, consumer confidence is at an all-time low, and job security for many Australians is in jeopardy (if they haven’t already been affected).

This has translated to a high degree of uncertainty, and fewer people are committing to a purchase. Real estate agents are reporting that buyer enquiry has fallen sharply.

Sellers are equally reluctant to participate in the market, with new residential listings having fallen 40 per cent since mid-March.

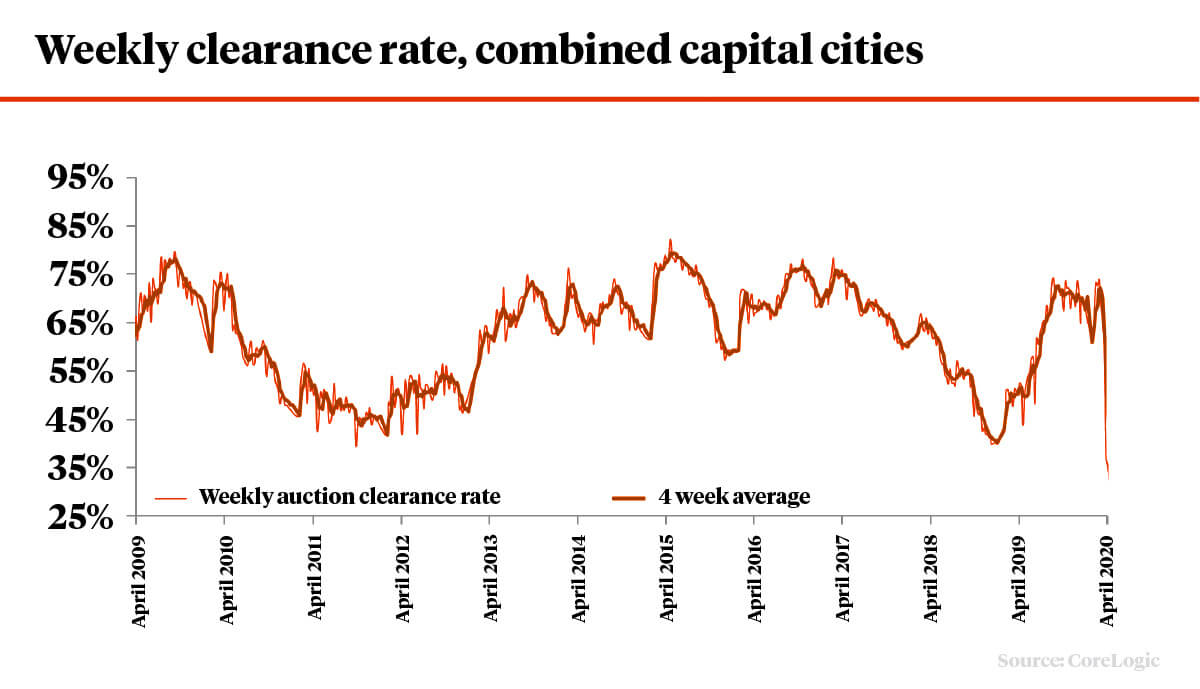

2. Auction Clearance rates are falling to near record lows

Social distancing rules have banned property open houses, and auctions have had to move online. Since this happened at least 400 of the nearly 1260 auctions originally scheduled for the last week of March shifted to non-auction listings.

The weekly average clearance rate across capitals now sits at 30.6 per cent – the lowest result in CoreLogic’s reporting history.

The fall in clearance rates is in part due to the shift towards private treaty sales, which accounted for 61 per cent of last week’s sales.

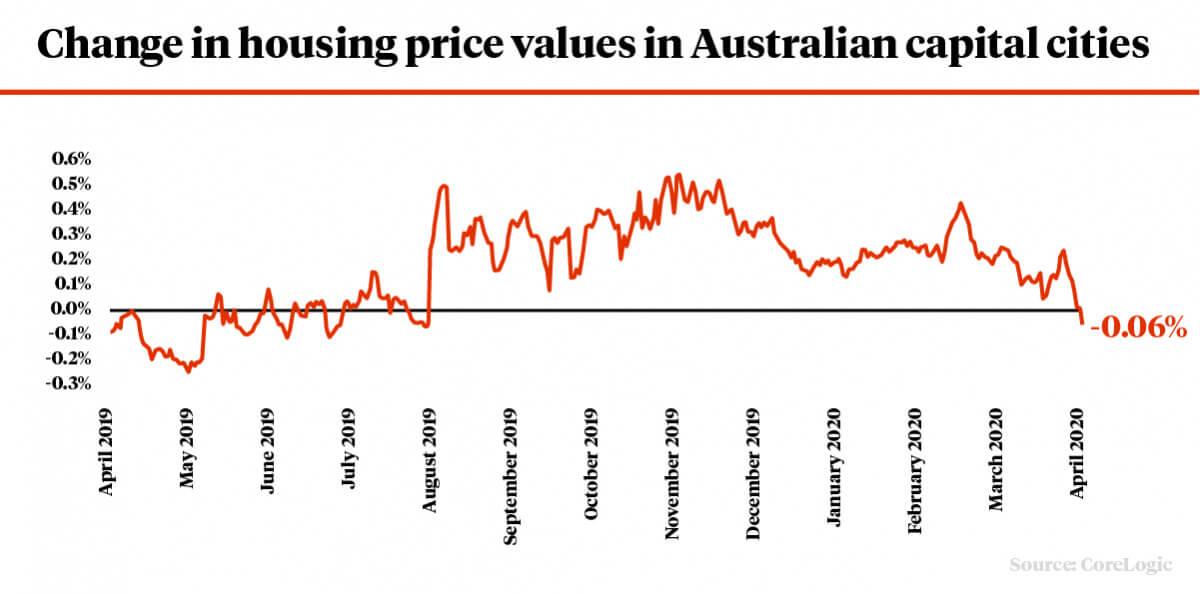

3. Property prices have already started to fall

Property prices have fallen on a week-to-week basis for the first time since August 2019.

CoreLogic analysis reveals growth in average house prices has been falling for the past three weeks and has now dipped into negative territory.

As the chart below shows, the three-week downturn coincides with the federal government’s shutdown of non-essential services and ban on physical auctions and inspections.

How far are house prices likely to fall?

We’ve already seen a drop in house prices due to coronavirus, but how far are they likely to fall? And for how long?

It’s a hard question to answer – economists are predicting anywhere between a 1 per cent drop in a best-case scenario, all the way to a 30 per cent drop in a worst case scenario. While opinions vary, most economists are predicting a price drop of around 10 per cent.

It all hinges on how well we are able to control the spread of the virus.

If the number of new cases drops to zero by the end of April and we don’t experience a second wave of infections after restrictions are lifted, then we’re likely to see only a minor impact on property prices.

Things are looking encouraging at the moment, but we’ll have to wait and see how things go.

What types of property will be most affected?

The effect of COVID-19 on property prices is not going to be uniform. Different areas will be affected based on employment and local economic factors.

In most cases, a downturn tends to affect higher-priced properties more than lower-priced properties. Here’s what has happened in the past:

- Expensive and higher-end markets will be affected the most.

- Prices might decrease in cheaper, blue-collar suburbs where employees can’t work remotely or there are chances of unemployment.

- Regional markets that do not depend on tourism and hospitality might not suffer as much.

- Well-located homes in middle-ring suburbs might hold their values.

How long will it last?

The short answer to this one is – no one knows. The economic situation is dynamic and affected by many factors, which makes the duration of this crisis impossible to predict.

Most experts are commenting that this is a short-term event and that the housing market will bounce back quickly once this is all over.

Again, it all hinges on how well we are able to control the spread of the virus, and how quickly we can get our economy up and running again.

What will happen to property prices after the pandemic?

Property price growth is expected to skyrocket following the coronavirus crisis, if past economic recoveries are anything to go by.

Experts are forecasting house values to shoot up at the end of the pandemic, which is consistent with what tends to happen after economic shocks.

The last time Australia had a recession was 29 years ago – and real estate led the rebound out of the downturn back then.

AMP Capital chief economist Shane Oliver has said:

“I suspect that if the shutdown ends by mid year resulting in minimal second-round damage to the economy (eg unemployment contained to around 10 per cent) and prices falling say 5-10 per cent, then all the stimulus should see a pretty decent bounce in prices into next year of around 10 per cent or so. But if the shutdown goes for much longer, unemployment rises to say 15 per cent and prices fall say 20 per cent, the recovery may be much slower.”

Chapter 2. Buying First Home During Coronavirus [What Should you do?]

Now that you have an overview of the property market, it’s time to cover the most frequently asked question I’ve had lately: “What should I do if I’m a first home buyer?”

In this chapter you’ll learn how COVID-19 has changed the home buying process, and whether or not you should consider buying a home at this time.

Can I still buy a home during the pandemic?

Yes, you can. The home buying process has changed due to social distancing rules, but there’s nothing stopping you from buying a home.

In fact, if your job is secure and you’re looking to buy a home, now might actually be one of the best times to buy.

COVID-19 has turned our property market into a buyer’s market – meaning that there are fewer buyers you need to compete with. If you’ve found yourself being priced out of the market in previous times, this might provide you with the opportunity you need.

On the other hand, if your finances aren’t secure – especially if you or your partner have lost your job – then it might be best to hold off on buying until the economic situation is a little more stable.

Tips for buying a home during coronavirus

While this can be a good time to buy, we are in an uncertain situation so you should take extra care to make sure that you’re making the right decision. Here’s what you should consider:

Make sure your job and income are stable

Banks and lenders are performing extra employment checks prior to settlement. Make sure that your job is secure and that your income is stable. You may even want to get an employment letter from your employer to confirm your employment status.

Get pre-approved before making an offer

Banks and lenders are tightening their policies at this time, so it’s especially important to make sure you’ll be able to get a home loan. Talk to a mortgage broker who will help you review your situation and find you the right lender.

Work with a buyer’s agent

A buyer’s agent will help you build a shortlist of suitable houses and – most importantly – will help you arrange private inspections of the properties you are interested in.

Negotiate on price

House prices have already started to decline in some areas. Make sure that you do a thorough property valuation to make sure that you don’t overpay.

If you negotiate well, you may be able to secure a 5-10 per cent discount on asking price depending on the type of property and location.

How to do a property inspection during COVID-19

The Australian government has banned open inspections of property from 25 March 2020, but you still have plenty of options for doing a property inspection

Options like virtual tours and digital walk-throughs are becoming more popular. These are a great way to get a good look at the property without worrying about catching or spreading coronavirus.

And while open inspections are banned, private inspections are still allowed, provided that the home buyer and agent follow the government guidelines.

These include:

- ✅ Maintaining an appropriate distance between each other

- ✅ All internal doors must be open

- ✅ Surfaces must be wiped down and disinfected, especially high touchpoints like doorknobs, table tops, kitchen surfaces, light switches, etc.

- ✅ The home buyer should not touch anything in the home.

Will I still be able to get a loan?

In response to coronavirus the lenders have become a bit more conservative about approving loans.

If your income hasn’t been affected, or you are working in a job that won’t be impacted by changes to your income – like a nurse, teacher, or in an industry that is booming – you will be in a strong position to get your home loan application approved.

But if you are on casual or contract income, it might be more challenging to get approval as they consider you a higher risk of losing your income.

What has changed?

Lenders are going to be a bit more conservative when they are assessing your income.

They want to be sure you can afford your loan repayments, and are especially critical for irregular income like:

- ⛔️ Contractor Income

- ⛔️ Commission Income

- ⛔️ Overtime

- ⛔️ Casual Income

- ⛔️ Bonus income

While some banks have left their policies unchanged, some have reduced the amount of casual/bonus/commission income that they will rely on your application.

In the case of overtime or bonus income, they previously used 80% of the gross income and now will only use 60% which can reduce how much you can borrow.

I’m already pre-approved. Will I have any problems?

Lenders have started reviewing pre-approved mortgages to make sure that you aren’t going through financial hardship due to the loss of jobs or reduced hours.

If your employment or income situation has changed significantly since your pre-approval, your lender may withdraw the approval. They can even do this on the day of settlement if they are concerned that you will not be able to afford the loan.

So if your job and income are stable, you should be ok. But if your hours are reduced or you have lost your job, you might be in trouble. Talk to your broker or lender to review your situation before you start making any offers on homes.

Employment checks prior to settlement

Some lenders have started doing employment checks just a day or two prior to settlement. If you fail this employment check, then you may lose your deposit and be unable to complete your property purchase. This can happen even if your loan has been approved!

Typically, this check is either:

- ⚠️ Calling you and asking if you are still employed

- ⚠️ Calling your employer

- ⚠️ Requiring a recent payslip

- ⚠️ Asking you to fill in a short form with 2-3 questions about your financial circumstances

In light of this, we highly recommend that you confirm your employment stability with your employer before buying a property. The best thing to do is confirm your employment status via a letter.

Chapter 3. Can I still refinance my home loan?

This chapter is all about refinancing your home loan during COVID-19

In this Chapter you’ll learn about the benefits of refinancing your loan and what to look out for when refinancing.

What are the benefits of refinancing my home loan during the COVID-19 pandemic?

1. Increase your loan and take cash out

If you have built up some equity in your property, refinancing will allow you to release that equity so you will have some cash on standby. You may also qualify for a cashback of up to $4,000.

2. Consolidate your debt

Pay out your credit card and personal loans under your mortgage. Pay off all of your debt with one home loan repayment and a single, lower interest rate.

3. Reduce your home loan repayments

You may be able to refinance your loan to get a lower interest rate or switch to an interest-only loan which will reduce your repayments even further.

You can either save the extra money, or make additional repayments which will reduce your loan term and reduce the amount of interest you have to pay.

What should I look out for when refinancing?

The most important thing to check before refinancing your home loan is to make sure you’re actually going to be better off with a new loan.

Refinancing does come at a cost, so it’s important to be aware of the expenses involved. Often these costs are minor compared to the money you can save, but you need to check.

You should also consider the type of home loan. Look for a home loan that offers flexibility such as offset or redraw facilities as these will help you pay off your mortgage faster.

Think about whether to fix your interest rate. Fixed rates are currently lower than variable rates so it may be a good idea to fix your rate. But it’s not always that simple. If you’re thinking about fixing your rate, head to Chapter 5 where we will cover this more in depth.

Finally, you need to consider whether or not you will be approved for a refinance. If you’re going through financial hardship, it can be difficult to get a refinance loan approved. In this case, you may be better off looking at your options for mortgage relief (covered in the next chapter).

You need to take action as soon as possible

We don’t know how long the window of opportunity for refinancing your loan will be open, so if you’re thinking about refinancing your loan, you should talk to a broker as soon as possible.

While we remain hopeful that our economy is going to reopen soon and that the current level of restrictions is as bad as it will get, there’s always the possibility that things could get worse.

If we see another spike of coronavirus cases, Australia may end up in total lockdown which could cause lenders to stop lending.

Read More: 7 Reasons to Refinance Your Home Loan in 2020

Chapter 4. Quick Guide to the Banks’ COVID help packages

In this chapter, you will learn all about the mortgage relief schemes that are available to you during the crisis.

If you’re facing financial difficulties due to the coronavirus, this chapter will help you to understand your options.

What mortgage relief schemes and options are available?

Banks and lenders are helping customers who are facing financial difficulties in the following ways:

Deferring scheduled loan repayments

All major lenders are allowing you to stop your mortgage repayments for between 3 to 6 months. These deferred repayments are also known as a mortgage freeze or a repayment holiday.

This may provide you some much-needed relief if you’re struggling, but it’s not without a catch. The interest will continue to accrue during the period of the repayment holiday and you’ll need to pay it off once the repayment period begins again.

Offering interest-only repayments.

Switching to interest only will reduce the size of your payments and can help relieve some of your financial strain.

While this can be very effective at reducing your repayments in the short term, you will end up paying more in interest over the term of your loan. Your repayments will also end up higher after the interest-only period ends, although we hope that things will be back to normal by then.

Usually, lenders and mortgage brokers are required to confirm your income when switching to interest-only repayments, but under the current circumstances this is not a requirement.

Access money in redraw

If you are ahead of your repayments on your loan, and your loan has a redraw facility, you may be able to access these funds and transfer them to your loan account.

This may help you avoid the need to apply for a repayment deferral.

Waiving fees and charges.

Lenders are adding overdue repayments to the balance of your loan, so you are no longer in arrears and being charged late fees.

Extending the loan term to reduce the amount of repayments.

If you only have 10 or 15 years left on your loan, it’s worth considering extending the loan term. Extending the loan term out to 30 years will reduce the size of your repayments.

The downside of doing this is that you’ll end up paying much more interest and may not fully pay off the loan before you retire.

If you decide to extend your loan term, it’s a good idea to shorten the term again once your in better financial shape to avoid the above issues.

Which banks are putting mortgages on hold?

All of the major banks and lenders are allowing you to pause your mortgage repayments. To get the most up to date information, go to your bank’s website.

| Bank of China | BOC COVID-19 |

| Bank of Melbourne | BOM Financial Hardship |

| Bank of Sydney | Bank of Sydney Hardship |

| Bank SA | Bank SA COVID-19 Support |

| Bankwest | Bankwest Coronavirus Support |

| BOQ | BOQ Covid-19 Support |

| CBA | CBA Financial Hardship |

| ING | ING Financial Hardship |

| Macquarie | Macquarie Coronavirus Support Hub |

| NAB | NAB Financial Hardship |

| Pepper Money | Pepper Money Hardship |

| St George | St George Coronavirus Support |

| Suncorp | Suncorp Financial Hardship |

| Westpac | Westpac COVID-19 Help |

For a complete list of the different banks and their COVID-19 hardship packages visit the Australian Banking Association.

Do I need to provide any type of proof to my bank?

It depends on your bank’s policy. Some banks are considering each request on a case by case basis, while others will allow a repayment pause without any evidence.

If your lender does require proof, a doctor’s note or a severance form should suffice.

Chapter 5. Questions to ask before fixing your home loan

In this chapter I’m going to cover all of the questions you should ask before fixing your home loan.

You’ll learn why fixed rates are at their lowest in Australian history, and how to know if fixing your home loan is a good idea.

Is now the right time to fix your home loan rate

The COVID-19 outbreak has caused the RBA to drop interest rates.

How low are fixed rates?

Fixed rates are the lowest they’ve been in Australian history. The big four are offering two-year and three-year fixed rate home loans at either 2.19 or 2.29 per cent.

Why are fixed rates cheaper than variable rates?

The Reserve Bank of Australia (RBA) cut the cash rate twice in March to a historic low of 0.25%. This represented a drop of 0.5%, but many lenders have only passed 0.25% of this rate drop to their variable home loan customers.

On the other hand, fixed interest rates have dropped as much as 0.8%.

Only the lenders themselves can tell you the exact reason for this, but it’s probably got a lot to do with the cheap 3 year bonds that our government has issued to the banks. Basically, the banks can secure funds at a rate of 0.25% for up to three years, so they can offer you a cheap rate while still maintaining their margins.

If fixed rates are lower than variable rates, won’t rates be falling?

In the past, if fixed rates are below variable rates, it means that the banks are predicting interest rates to fall.

But in this case, that seems unlikely. At 0.25%, the official RBA cash rate is already at the lowest in history. While the RBA could potentially do one more rate cut, most economists believe this is very unlikely.

How do I know if fixing is a good idea for me?

Even with these amazing rates, fixing your home loan isn’t for everyone. Here’s what you need to ask before fixing your home loan:

Are you planning on making extra repayments?

Your ability to make extra repayments may be limited during your fixed rate period, or you may be charged a fee.

Is there any reason you might want to leave the loan early?

If you’re thinking about selling your property or refinancing during the fixed rate period, you’ll need to pay break fees. These can potentially cost thousands of dollars. So if you’re planning on leaving the loan early, you may want to stick with a variable loan.

Do you want an offset account or redraw facility?

Some lenders don’t offer an offset account or redraw facility for fixed rate loans. In some cases, they only offer a partial offset which is nowhere near as useful as a full offset account.

What is the revert rate?

The revert rate is the interest rate that your loan moves to after the fixed term ends. These revert rates are typically higher than a standard variable rate, so you’ll need to be prepared to renegotiate your loan at the end of the fixed term to make sure you’re getting a competitive interest rate.

Do you want flexibility or certainty?

This is the ultimate question when it comes to deciding whether to fix your home loan rate. A variable interest rate will offer you more flexibility – better facilities, the ability to make extra repayments and the ability to refinance your loan if a better deal comes along.

A fixed rate loan means that you know exactly what your repayments are going to be for the duration of the fixed term. That makes budgeting easier, and with fixed rates where they are right now, helps you to save some money.

Read More: Is now a good time to fix my interest rate?

Are break fees a risk?

If you exit your fixed rate loan early by refinancing, selling your property, or paying out your loan, you may need to pay a break fee.

The break fee is supposed to reimburse the lender for their economic loss, as they have borrowed the funds that they are lending to you at a fixed rate as well.

Under the current circumstances, your lender may actually benefit if you repay your loan early, but that doesn’t mean they won’t try to charge you a break fee. So we don’t recommend fixing your home loan if there’s any chance you will need to exit your loan early.

Read More: Get in touch with our Mortgage Brokers to see if you are eligible for these fixed rates.

Chapter 6. Frequently Asked Questions (FAQs)

In this I’m going to answer all of the FAQs I’ve been getting from our customers.

If you have a question that hasn’t been answered in the article so far, it should be answered here.

What is financial hardship?

If you have a home loan and you’re struggling to make repayments for a specific period of time, this is considered to be financial hardship.

I’ve lost my job, or lost hours as a result of COVID-19, what type of financial hardship reliefs are banks offering?

Banks are giving customers the option to pause their home loan repayments for up to 6 months. Depending on your lender, you may also be able to access assistance options such as:

- Switching to interest-only repayments

- Extending your loan term

- Waiving fees on early term deposit withdrawals

- Interest rate freezes on loans

- Emergency credit card limit increases

Will deferring loan repayments affect my credit rating?

No. The Australian Prudential Regulation Authority (APRA) has noted that repayment holidays would not count as “mortgage in arrears” so it would not be recorded on your credit file.

However, this is only applicable if you have previously been meeting your repayment schedules and chose to take up the offer of a repayment holiday due to COVID-19.

Will I be charged interest if I get a repayment holiday?

Yes, interest will continue to accrue during the repayment holiday period. This is called interest capitalisation.

The additional interest can be paid off by increasing your repayments once your repayments begin again, or extending the length of your home loan. You will need to discuss this with your bank to select your preferred option.

Can I still get a repayment holiday if I have funds in my redraw?

Yes, you should be able to. But it might not be in your best interest since the interest on your loan will be capitalised if you get a repayment holiday. In most cases you are better off using the funds in your redraw to cover your repayments.

In case of a joint account, can one of us apply for a mortgage freeze since only one of us is experiencing financial difficulty?

Yes, you can. Even if there’s only one person who’s experiencing financial hardship, you can still apply for a repayment holiday.

Can I use early access to super to make mortgage repayments?

The government is allowing early access to your super if you have lost your job or income due to the coronavirus. This is interest-free and you won’t be taxed on the amount you’ve withdrawn from the super. You can access up to $20,000.

This is not technically part of the mortgage relief scheme, but you can use this money to make repayments on your home loan.

However, this is the last option you should choose if you’re suffering from financial hardship. Accessing your super means that you will have reduced funds for retirement.

Should I wait for the banks to contact me if I’m struggling with my repayments?

No, you should reach out to your lender as soon as you realise you may have trouble with your repayments. The earlier you talk to your lender, the more assistance they will be able to give you.

Who do I contact and how if I’m in need of financial relief from my lender?

There are many ways you can contact your bank or lender, but your first choice should be online via their website or smart phone app.

You can call them but due to the high number of calls during this period, you might have to request a call back.

Chapter 7. How we can assist

In our final chapter, I’ll cover how we can help you during this challenging time.

How can we help as mortgage brokers?

Our mortgage brokers are working overtime to help our customers during this period. We are constantly monitoring the position of lenders so we can still get your loans approved during this time.

Some of the ways we can help include:

- ✅ Advice on buying a new home

- ✅ Helping you with your existing mortgage

- ✅ Refinancing to a lower interest rate or interest-only repayments

- ✅ Releasing equity to help with cashflow

- ✅ Consolidating debt and reducing repayments

Call us at 1300 088 065 or fill in our free assessment form if you need our help in any way.

Start again

Start again