15 minute read

15 minute read 1. What is the first home super saver scheme?

First Home Super Saver Scheme (also known as FHSSS) is a government scheme made to assist you with speeding up the time it takes to save a deposit and buy your first home.

FHSSS uses voluntary before-tax contributions made to your superannuation fund. You can then withdraw these funds to use later as a deposit towards buying your first home.

Example:

Bianca has been working as a Marketing Associate, makes $50,000 per year and wants to use the FHSSS to speed up the time it takes to save for her first home purchase. She has never owned a home before and wants to buy a place as soon as possible but has no savings.

Bianca asks her work to take voluntary before-tax contributions of $10,000 per year from her salary and make them to her superannuation fund. This works out to roughly $833 per month from her before-tax pay.

This money is being taken before tax, which reduces how much tax she pays per year on her total pay. In effect, Bianca’s take-home pay (i.e. the pay she receives in her bank account every month) is only reduced by $6,400 per year or $533 per month!

Using the First Home Super Saver Scheme, Bianca saves around $300 more per month.

After 3 years of saving, based on the First Home Super Saver Scheme Calculator, Bianca would have an estimated $25,608 available for a deposit because of the FHSSS. This is $6,089 MORE than if she had been saving in a regular deposit account!

2. Why use the First Home Super Saver Scheme (FHSSS)?

The First Home Super Saver Scheme makes it easier for you to save your deposit by making before-tax contributions to your superannuation. Using the FHSSS, you can automate saving for your deposit by portioning a part of your income to be put into your super account before tax.

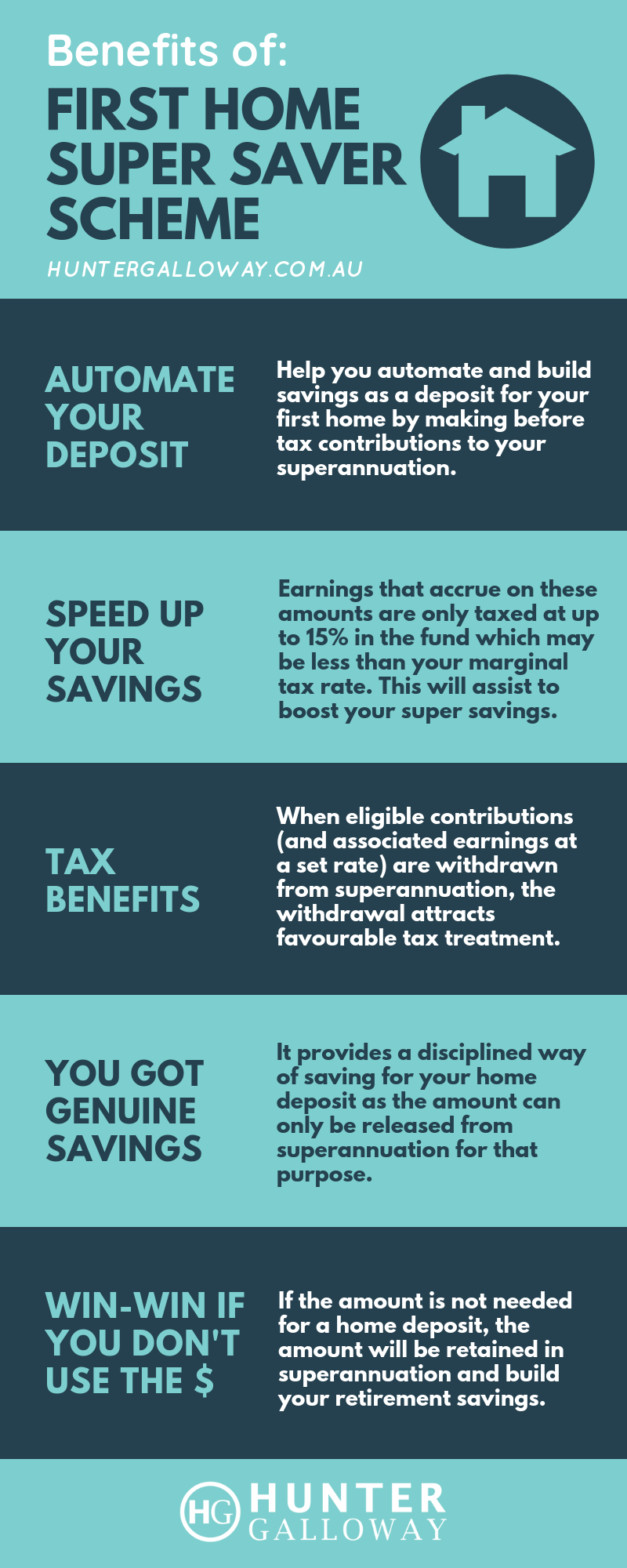

What are the benefits of using the First Home Super Saver Scheme?

- Speeding up your savings. Any earnings that you make on contributions to the First Home Super Saver Scheme are taxed at 15% in your superannuation fund. This can assist with speeding up your savings because this tax rate is likely less than your marginal tax rate.

- Tax benefits. You get favourable tax treatment on eligible funds that are withdrawn (and any earnings associated) from your super.

- Meeting genuine savings criteria. Putting your savings on autopilot and having them in the FHSSS makes them genuine savings in the eyes of the banks.

- Win-win even if you don’t use the funds. If you do not use the funds to buy a home, you can keep them in your super fund and help build for the future.

Can I use my super for a house deposit?

The First Home Super Saver Scheme does not allow you to use your regular super contributions towards your house deposit. You can only withdraw the additional contributions you make as a part of the FHSSS to buy your first home.

The only situation where you can use your normal super for a house deposit is if you have set up a self-managed superannuation fund (SMSF) and you buy a house as an investment property. You can’t use normal super funds to buy a property to live in.

3. How does the First Home Super Saver Scheme work?

People who have never owned property in Australia can make extra contributions to their superannuation (known as voluntary contributions) from their pre-tax income to build a deposit for a home. You reduce your take-home pay but increase the amount your employer puts into your super.

So the FHSSS works by reducing the tax you pay from your salary and (should) help you save a deposit for a home quicker.

Example:

Sally has been working as an Advertising Associate for the last 3 years and earns $70,000 per year. She wants to buy her first home as soon as possible. So, she will make the maximum annual salary sacrifice of $15,000 per year over 2 years.

Sally’s salary sacrifice contribution of $15,000 will reduce her take-home pay by only $9,650. After 2 years, she will have an estimated $25,355 available for deposit under the First Home Super Saver Scheme. That is $5,802 more than Sally would have had if she had been saving in a standard deposit account!

Suppose Sally wanted to reduce the salary sacrifice amount and increase how much money she took home. In that case, she could reduce her annual salary sacrifice contribution to only $10,000, which would only reduce her take-home pay by $6,450.

After 3 years of saving, Sally would have an estimated $25,892 available for deposit under the FHSSS, which would work out to be $6,210 more than if she had been saving in a regular savings account.

Calculations based on figures from First Home Super Saver Scheme Calculator

4. Who can apply for the First Home Super Saver Scheme?

Similar to the First Home Owners Grant, to be eligible for the First Home Super Saver Scheme, you must meet the following criteria:

- You cannot have owned property in Australia in the past.

- You need to be over 18 years old.

- You must be planning to live in the property for at least 6 months within the first 12 months of owning it.

- You must not have used the FHSSS before.

The Australian Taxation Office (ATO) says eligibility is based on an individual basis. This means that couples, siblings and friends can still access each of their own FHSSS contributions to purchase the same property. Also, if your co-purchaser has previously owned a home, it will not stop you from applying if you are eligible.

Example:

Andrew and Steve want to buy a property together. Andrew has owned property in Australia in the past and is ineligible for the FHSSS, but Steve has never owned property in Australia before.

Steve meets all the criteria for the FHSSS, so he can apply for the concessions in his own right and is not affected by Andrew having owned property in the past, even though they will end up buying a property together in the future.

There are some exceptions to the eligibility, including financial hardship provisions. If you have previously owned property but have suffered financial hardship that has resulted in a loss of ownership (including bankruptcy, divorce, loss of employment, or illness), you could be considered for the First Home Super Saver Scheme Hardship Application.

Read More: First Home Owners Grant Conditions for Queensland

5. How much can you save using the first home buyer super saver scheme?

There are limitations on the amount you can save using the First Home Buyer Super Saver Scheme. There is a maximum voluntary contribution of $15,000 per financial year or up to a maximum of $30,000 in total.

Voluntary contributions can either be concessional contributions from pre-tax income like salary sacrifice or personal contributions in which tax deduction can be claimed.

Non-concessional contributions can be made from after-tax income, and no-tax deduction can be claimed.

Concessional contributions include salary sacrifice contributions and are taxed at 15%, but the non-concessional contribution is made from your after-tax pay, so you will pay your regular marginal tax on these.

There are different caps to concessional and non-concessional contributions, which you can discuss with your accountant and financial adviser.

Donald is employed full-time and receives $115,000 taxable income per year. He wants to make the maximum salary sacrifice contribution possible which will be limited to $15,000. He asks his employer to take a $15,000 annual salary sacrifice contribution, which will reduce his take-home pay by $9,150. After 2 years of saving through the FHSSS, there will be approximately $24,327, which is $5,804 more than if he had been saving with a regular account.

6. How much can you have released from the FHBSSS?

The amount you can release is limited and depends on the type of contribution you made to the fund. If you made a non-concessional contribution, 100% is eligible to be released, and if you made a concessional contribution, 85% of the amount is eligible to be released.

Remember that the maximum amount that can be released is not the actual amount you will receive from the ATO. They will withhold the appropriate amount of tax and offset your balance against any outstanding Commonwealth debts.

7. First Home Super Saver Scheme Calculator

You can check out the First Home Super Saver Scheme calculator to determine if FHSSS is right for you.

The benefits of the First Home Super Saver Scheme will depend on your taxable income and annual sacrifice amount. The ATO’s calculator can help you determine the total benefits.

The First Home Super Saver Calculator compares different scenarios when saving for your first home using your annual pre-tax contributions to superannuation of up to $15,000 per year, up to a maximum of $30,000, less your tax rate in a regular savings account.

Steps in using the First Home Super Saver Calculator:

- 1. Enter your taxable income

- 2. Enter how much you would like to save (or salary sacrifice per year)

- 3. Look at the total benefit, and how many years it would take you to achieve this

Read More: How to Buy a House 🏘 (Step-By-Step Case Study)

8. How do you pay extra money into my super for the FHSSS?

As covered above, you can make extra payments (called voluntary contributions) to your superannuation fund with the intention of using those funds toward your first home.

Can I use salary sacrifice to save for a home deposit?

If you are paid through an employer (i.e. you get payslips), you can ask your employer to reduce your take-home pay and increase your pre-tax contributions to your existing superannuation fund. These are taxed at 15%, along with deemed earnings and can be withdrawn as your deposit.

On the other hand, if you are self-employed, you can make contributions to your superannuation fund and claim a decision on the personal contributions later. You need to be mindful of staying within the concessional contribution cap.

In either case, you do not need to let the superannuation fund know that you plan on participating in the First Home Super Saver Scheme. You only need to make these extra voluntary contributions. Then when you are ready, you apply to the ATO to release the funds.

9. How do you withdraw money from the FHSSS?

There are a few steps in withdrawing your voluntary superannuation contributions from your fund, and your first point of call is actually the ATO—not your superannuation fund.

The steps in withdrawing your money contributed to the FHSSS are:

- Apply to the Commission of Taxation for the ‘FHSSS determination and release’ via your myGov account.

- The Commissioner will process and provide your ‘FSSS determination’.

- Then you need to apply to the ATO to release your funds.

- The ATO will then release an authority to your superannuation fund, who will send a request to release the amount to the ATO.

- The ATO will then calculate and hold back any tax you owe and offset against any outstanding Commonwealth debts.

- The ATO will then send the balance of funds to you.

The FHSS scheme maximum release will take into account your $15,000 financial year limit and $30,000 total limit when calculating how much will be refunded to you.

Also, know that you can only apply for a release once, so you want to have confirmed you are ready to buy a property before going through this process.

10. How long does it take to get funds released from the First Home Super Saver Scheme?

Because there is a fairly lengthy process to get your funds released under the FHSSS, it can take around 20-25 business days for your superannuation fund to release your deposit funds and pay them to you.

This is on top of the 10-20 business days it can take the Commission of Taxation and ATO to arrange their determination and other paperwork.

Read More: First Home Super Saver Scheme Guide.

11. Is there a time limit to use the funds released from the FHSSS?

Yes, once the savings have been released, you have up to 12 months to sign a contract of sale or construct a home.

You need to be purchasing a residential property to live in, and it cannot be:

- Any premises not capable of being occupied as a residence—for example, a shop.

- A houseboat

- A motorhome

- Vacant land *** (see below)

Unfortunately, you aren’t able to buy a houseboat using the First Home Buyer Saver Scheme…

***If you want to buy vacant land to build a home on you need to have entered a contract to build the house within 12 months of the funds being released to you.

Example:

Sabrina has withdrawn funds from her FHSSS to buy vacant land to build a house on. The funds from her FHSSS are released on 1st November 2020. She signed the contract of sale to purchase the land on 1st December 2020 and then took 6 months to sign a contract to build the home.

The contract to build the house was signed on 1st July 2021. Sabrina entered a contract to build the house within 12 months of the FHSSS funds being released, so she is ok.

12. What happens if I do not use the FHSSS funds within 12 months?

If you do not sign a contract to buy a home or construct a property within 12 months from the funds being released from the FHSSS, you can either:

- Request an extension of up to 12 months.

- Recontribute the total amount of funds back into your superannuation. This needs to be a non-concessional contribution and be at least equal to your assessable FHSS released amount, less any tax withheld.

- Keep the released amount and be subject to FHSS tax, a flat tax of up to 20% of the FHSS released amount.

Read More: First Home Super Saver Scheme Fact Sheet

13. What are the risks with the FHSSS?

As with any government scheme or offer, there are going to be some benefits and risks:

- You need to make (additional) voluntary contributions to the FHSSS, and these cannot be made on your behalf—like your regular employer superannuation contributions or contributions made by your spouse.

- To remain eligible under the First Home Super Saver Scheme, you are limited to a maximum of $15,000 contribution per financial year and a total amount of $30,000. Go above this amount, and you will get slapped with massive tax penalties.

- The ATO will determine how much you can withdraw after taking into consideration the total contribution amounts and tax. So you actually will not withdraw the total amount you have saved.

- Once you withdraw the funds from the FHSSS, any concessional contributions and associated earnings will be included in your assessable income and taxed at your marginal tax rate, less a 30% tax offset. Non-Concessional contributions are tax-free because they were already taxed going in.

- You need to sign a contract of sale or construct a home within 12 months of withdrawing the funds from your superannuation account, and you need to live in the property for at least 6 months.

Ultimately, being able to withdraw the funds will be at the ATO’s discretion, and as you can expect, they will hit you with heavy penalties if you make any false statements.

Bonus 1: Can the FHSSS be used with the $15,000 First Home Owner Grant?

The good news is that yes, the First Home Super Saver Scheme can be used in conjunction with the First Home Owner Grant and Great Start Grant in Queensland, provided you meet the eligibility criteria:

- You have not previously owned a residential property.

- Your minimum age should be 18 years, and you must be a permanent resident of Australia.

- The value of the house, including the land, is less than $750,000.

- You must be buying or building a brand new home.

- You must move into the new home as your primary home within 1 year and live there continuously for 6 months.

In Queensland, the $15,000 First homeowner grant is currently used for brand-new or nearly constructed properties. So, if you can use the First Home Super Saver Scheme and save up $30,000 over two years, then add that to the $15,000 from the government grant, you’re basically up to $45,000 to put towards your first home!

Example:

In the example above, Sabrina has withdrawn funds from her FHSSS to buy vacant land to build a house on. The funds from her FHSSS are released on 1st November 2020, and she signs the contract of sale to purchase the land + the contract to build a home on 1st December 2020.

Sabrina had never owned property before and planned on living in the home for at least 6 months. The value of the new house, including the land, was less than $750,000, and she met the other criteria above, meaning she also qualified for the $15,000 First Home Owner Grant.

You can check your eligibility for the first homeowner grant here.

Read More: Queensland First Home Owners Grant

Bonus 2: What do the banks consider as genuine savings?

Genuine savings show the bank that the applicant has a bit of skin in the game, a bit of hurt money that you have saved up yourself. While most banks consider the First Home Super Saver scheme genuine savings, they will also count any of the following:

- Savings held or accumulated over 3 months.

- Shares or managed funds held for 3 months or greater.

- Equity in real estate or property.

- Term deposits held for 3 months or greater.

- First Home Super Saver Scheme (FHSSS).

- Some lenders allow exceptions if rent has been paid on time for the last 3 months or greater.

Read More: What Is Genuine Savings?

Bonus 3: First Home Super Saver Scheme vs Super Home Buyer Scheme.

The Home Super Scheme is a government grant allowing you to access your super up to and including 40% or no more than $50,000 to buy your first home. So if you are a first home buyer and have saved a 5% deposit, you can use this scheme to bump up your deposit and get a property sooner.

The Home Super Scheme is different from the First Home Super Saver Scheme in the following ways:

- You are borrowing from your super. With the Super Home Buyer scheme, you are essentially borrowing money from your super, and you will have to pay it back based on capital returns if you sell the house. But with the First Home Super Saver Scheme, you are making extra contributions and then withdrawing them, so you don’t have to pay it back.

- No property price cap limits. The Super Home Buyer Scheme does not have any limits on the value of the property you can buy. With the First Home Super Saver Scheme, the home you’re buying should not be worth more than $750,000, including the land it is on.

- Higher withdrawal limit. Under the First Home Super Saver Scheme, you are limited to a maximum of $15,000 contribution per financial year and a total amount of $30,000, and if you go above this amount, you will get slapped with massive tax penalties. But with the Super Home Buyer, you can access up to $50,000.

- No limitation on citizenship. The scheme is not only for Australian citizens, as is the case with other government schemes. That means if you are a permanent resident, you can qualify for this scheme.

The beautiful thing with the Super Home Buyer Scheme is it’ll help those hard-working first homeowners that don’t quite qualify for the other government grants either because of income limits or because they’re not citizens.

Important: According to the ATO website, the $50,000 limit on eligible contributions will only apply to requests for FHSS determinations made from 1 July 2022.

Next steps and settling your new home

Our team here at Hunter Galloway is here to help you buy a home in Brisbane.

Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts to help make your home loan journey as simple as possible.

The Hunter Galloway Mortgage Broker Brisbane team is here to help. We have a team of home loan experts.

If you want to get started, give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Further reading for Home Buyers

- For our comprehensive guide for First Home Buyers, check out this page.

- Looking at getting a loan? Check out our Complete First Home Buyers guide.

- Looking to buy a home in Brisbane? Check our Home Loan Guide to Brisbane

- Don’t forget the 16 hidden costs of buying, which we covered in detail here.

References:

Note: Information is current as of September 2022 and subject to change without any further notification. Any home loan application is subject to credit approval and verification of all supporting documentation. Consider this article as general in its nature and not to be taken as financial advice.

1300 088 065

1300 088 065

Start again

Start again