Have you had your home loan declined or knocked back by your bank?

Getting a home loan used to be such an easy experience. Now, it can just feel frustrating, and it’s mostly because of government forces that have been pushed onto the banks. If you are a first homebuyer and on a lower income, things are a bit trickier than they used to be when getting a loan, which could be one of the reasons you have been knocked back.

But it’s worth remembering that not all banks are the same!

They all have different lending policies, and if you are working with an experienced Mortgage Broker, you will be able to find a lender that will work with your situation.

To help you understand why your home loan was declined, we will take you through 15 reasons the banks knock back home loans.

Let’s dive in!

1. Failing The Bank's Scorecard

This is the number one reason why your loan could get declined. The reality is when you submit your loan application to the bank, they will complete an automatic internal score before they even assess your application.

This scorecard is a computer algorithm that looks at several things. It looks at your credit score, work history, and even how long you’ve lived at your current address. In many cases, if you fail the bank’s scorecard, the bank will flat-out decline your application, and you won’t get a second chance. The scorecard helps the bank identify risks associated with your application. The better the scorecard, the better your chances of getting a loan approval.

Although banks don’t openly advise how they credit score, there are things we’ve picked up over the years. Here are two things to help increase your chances.

- First, ensure there are no issues with your credit file. Defaults, judgments or bankruptcies will see you fail the bank’s scorecard. Some lenders are slightly more lenient with defaults as long as they’re under a few hundred dollars. You can grab a copy of your credit file through Equifax, illion and Experian. Equifax will give you a free copy of your credit file every 12 months.

- The second is to ensure that your application has as much information as possible. The more information provided, the better the bank’s scorecard. This means you must include all assets, such as vehicles, jewellery, tools, bikes, etc., in your position statement. Also, include your superannuation and any bank accounts that you have money in. It helps to include three years’ worth of history of where you’ve been living and even where you’ve been working. Adding all mobile numbers, landlines, emails, and even fax numbers will increase the scorecard results. It also pays to include your previous and current employer’s contact details, such as phone numbers and even addresses. Effectively, you want to ensure every data point the bank requests is provided to give yourself the best possible chance of increasing your scorecard.

2. The APRA Buffer Benchmark

This has been the biggest change that’s really cut a lot of people’s borrowing capacity. The banks have to check if you can handle your payments if interest rates jump up by 3%. This isn’t new. APRA bumped up the buffer from 2.5% to 3% back in October 2020, and they’ve kept it there. The buffer is designed to give you some room so that you won’t immediately be under mortgage stress if interest rates change.

Let’s say you are looking at a loan with, say, 6% interest. The bank will check to see if you can manage to pay at 9% interest. It’s a good thing in some ways, but it is also a bit frustrating because it cuts your borrowing power by about 5%.

The banks themselves have gone back to the regulator, saying, by our own models, we’re at the top of the interest rate cycle — it doesn’t look like the interest rate will get to 9%. But APRA said no, we still want this in place to have some extra checks and balances.

We can understand where they’re coming from because people are starting to feel a bit of the strain from 13 interest rate rises, and if APRA didn’t have these buffer rates in place back then, the situation right now would be even more dire for some people.

However, if you’re reaching the top of an interest rate cycle and not going to go any further you wonder whether they’re just trying to make it more difficult to get a loan and whether they’re really doing the right thing.

So, one of the reasons your loan can get declined is because your income fails to meet this buffer.

3. Small Deposit

These days, you will need at least 8-10% of the property value as a deposit to get a home loan.

If you are putting down a minimal deposit, the bank is going to look at something called genuine savings. Now, the definition of genuine savings differs from lender to lender. Some lenders will need to see genuine savings if you’ve got less than a 15% deposit. Some other lenders only need genuine savings if you have a 10% deposit.

Your loan may get declined if you have a minimal deposit and no genuine savings.

Effectively genuine savings mean you must demonstrate to the bank that you’ve saved up 5% of the purchase price over 3 months or longer. So this is important if you want to purchase a property in the near future and you’ve been gifted funds. It might make sense to get the funds in your account earlier so you can show you held the funds in your bank account for three months or longer.

Another interesting thing is that banks can accept rental history from a licensed real estate agent. So, if you’ve got 12 months of good repayments on your lease, that can be considered genuine savings.

But it is key to remember that with rental history, they don’t use the amount you paid in rent as a deposit. You still need to have your 5-10% deposit. However, you don’t need to have saved it up progressively over time. Your parents can just gift you that money, which can be used as your deposit and your rental history will work as genuine savings.

In some cases, if you don’t have a high deposit but have demonstrated a propensity to save – that is, you are paying your rent and putting money away each week, the banks get comfortable knowing you can pay back the mortgage. For example, if your rent is $400 a week and you are also saving $150 a week, the lender will see that you can comfortably repay up to $550 a week towards the home loan. Now, if your mortgage repayment will be only $390 a week, then you are in a very good position, and the bank will gladly give you a loan.

An added bonus is if you’ve been in your role for two years, it demonstrates you’re quite stable in your employment and income and have a good savings history. We will cover income and employment in detail later.

It’s important to have your deposit and genuine savings in order.

BUT, there are situations where you can use a guarantor to help you borrow up to 100% of the property plus additional costs. Yes, that’s right, you can get a home loan with no deposit.

Best of all, you avoid paying lenders mortgage insurance, which is usually payable if you have less than a 20% deposit.

Again, the banks all have different credit lending policies, and a small deposit to one bank is completely fine with another.

Will I get higher interest rates if I have a small deposit?

A couple of years ago, it didn’t matter if you had a big deposit or a small deposit; everyone pretty much got the same rates. These days, if you have a 5% deposit, you are actually charged a higher interest rate because you’re seen as a bigger risk to the bank.

Interestingly, if you get assistance from the Home Guarantee Scheme — the 5% government scheme where the government acts as your guarantor— you get the same rates as if you got a 20% deposit. This is where having a broker to help you through this process can really help you find the best deal for your situation.

4. Low Valuation

Low valuation is a common problem we see with off-plan purchases and those looking to build. When purchasing an off-plan property, settlement often doesn’t occur until months or even years after the contract has been entered and unconditionally locked in. In this case, the bank won’t be able to value the property until the off-plan property has been completed.

Often, when valuers go out and value the off-plan purchase, they need to find comparable sales with recent properties that have sold in the area. This means they can’t use off-plan purchases as comparable sales; they must find established stock in the area. The downside is that this leads to valuers undervaluing the property.

Brand-new builds also experience the same problem. If you’re building in a new estate and there are no recent sales of properties like yours in the area, your property may be undervalued.

If your property is undervalued, it could result in additional costs for things like mortgage insurance or, worse, being unable to get your loan approved.

There are ways to mitigate this by having two or three banks value the property upfront. The difference between one valuer and another can be astounding. We’ve seen up to a $50,000 variance in a valuation for a property being purchased at $475,000. The lower valuation meant we couldn’t secure finance, but the higher meant we could get the job done. This is how much of an impact valuation can make.

Read More: How To Challenge A Bank Valuation

5. Being Over 45 Years Old

Although there are laws (check out the Discrimination Act) to make sure banks don’t discriminate because of your age, it is common for lenders to ask for an exit strategy in paying off your home loan if you are over 45 years old.

This retirement reality check is an interesting one because it’s not the kind of thing that you would think of if you weren’t working in the finance space. For most people, buying at 45 doesn’t feel like it’s a particularly old age, and they’re not thinking about retirement. It’s something that’s further ahead in the future for most people.

In effect, these restrictions can limit your mortgage options because of your age. If an exit strategy can’t be determined, then your loan could be knocked back.

While different banks have different policies, some common exit strategies for anyone aged over 45 years old are:

- Downsizing and moving to a smaller house once you reach retirement age

- Selling other investment properties or shares.

- Releasing funds from your superannuation to pay down the loan.

- Recurring income received from your superannuation fund.

Not all banks are the same here. Some don’t ask questions until you are 55 or even 60 years old.

6 Being Too Young

Don’t worry; the young people get grief too from the banks!

You can’t apply for a home loan if you are under 18 years old, but did you realise that being under 25 can negatively affect your credit score? Being young, you may have a very limited credit history or none at all to show you are a good borrower.

Sometimes, as a young person, your loan may be rejected because you are still in the early stages of your career, and therefore, your debt-to-income ratio may be too high for the bank, even if you have the potential to earn more in the future. We cover the debt-to-income ratio in detail below.

The good news is that not all banks use credit scores, and some may be willing to give you loans when you are straight out of school, especially if you are a medical professional. Talk to an experienced Mortgage Broker who will understand and help you navigate getting a home loan as a young person.

7. Spending Habits

When you apply for a home loan, nearly all banks will want to see your last 3 months (Suncorp Bank wants to see 4 months) day-to-day transaction account statements. The banks will look into your monthly living expenses to determine if you can afford to make your home loan repayments.

If you have private health insurance or school fees, the banks call these discretionary expenses outside their Henderson Index, which can reduce your borrowing power.

A couple of years ago, we’d say things like Netflix, fast food and shopping at Zara would affect your borrowing capacity (and for some banks, it does). However, with some banks, you can argue that, hey, over Christmas, I spent a lot of money on presents—I went out a lot that’s not going to be ongoing, and that can stop. The banks will accept that explanation for a few living expenses.

But with expenses like private health insurance, school fees and gambling, the banks just say, No, we won’t negotiate on this – you have to include these as ongoing expenses, and it could reduce your borrowing capacity or, at worst, get your home loan declined. Another one that we’ve seen recently is Onlyfans, where the banks see it similarly to a gambling expense, almost as a recurring thing. So, if you are on some of these platforms, be careful because the banks will ask you about them when it is time to do your home loan application.

This is an example of how some banks will categorise your monthly living expenses.

Monthly Living Expenses (detail expenses/costs) | |

Childcare | $1,000 |

Kids/Pets | $ 300 |

Clothing | $ 200 |

Education | $ 1,000 |

Groceries | $ 1,000 |

Insurances | $ 250 |

Investment | $ 500 |

Medical | $ 300 |

Other | $ 200 |

Owner Occupied Expenses (e.g. Rates) | $ 300 |

Recreation | $ 400 |

Connections | $ 400 |

Transport | $ 300 |

Rent/Board | $ 2,500 |

TOTAL | $ 8,000 |

Case Study: Spending Habits Reducing Borrowing Capacity

We had a client recently who was gambling. So there was a lot of money going in and a lot of money going out. The bank reconciled the ins and outs and said, well, every month, you’re actually going backwards $500, so we’re taking that into consideration on your living expenses. This additional expense impacted the client’s borrowing capacity by a few hundred thousand dollars!

So you need to be careful with your living expenses. The lenders are going to definitely take your spending habits into consideration.

Read More: Barefoot Investor Bank Accounts Explained.

8. Non-Disclosure

Forgetting to include a liability in your application, such as a credit card, could see you knocked back. Non-disclosure of liabilities isn’t the only thing the banks are looking for. Providing false or misleading information in your application could also see you getting declined.

In addition to the risk of rejection, intentionally providing inaccurate information can have legal consequences. Lying on a home loan application is considered fraud, which is a criminal offence in Australia. If you are found guilty of fraud, you could face serious penalties such as fines or even imprisonment.

Sometimes, you may feel tempted to bend the truth in order to increase your chances of getting approved for a home loan. However, it’s important to remember that banks have sophisticated ways of verifying the information you provide them. Hence, it pays to provide correct and accurate information when applying for your loan. Providing false information can harm your chances of approval and your financial future in the long run.

To avoid any potential issues, it’s best to be honest and transparent throughout the home loan application process. This includes disclosing all sources of income, debts, and other financial obligations. By doing so, you can increase your chances of being approved for a home loan and avoid any legal consequences that may arise from providing inaccurate information.

Read more: Explanation Letter: Written Sample And Template For Home Loan Application.

9. A High Debt Position: Debt-To-Income Ratio

Having too many credit cards, car loans, and personal loans reduces your chances of getting your loan approved. The banks assess your application based on how much of your income is going to pay your existing debts and new mortgage. This is called debt to income ratio, and the banks generally want it to be below six times.

Debt-to-income ratio or DTI is where the banks look at your income as a multiplier of your debt. These days, the banks will limit DTI to 6 times—that is, they will only lend up to 6 times your income. So, for example, if you earn $100,000, your maximum loan amount is $600,000, and if you try to borrow more than that, the bank will decline your loan.

In some cases, this depends on your deposit. So if you have a deposit of less than 10%, a lot of the bigger banks (and some smaller ones) will flat-out decline your loan if you want to borrow more than 6 times your income – no negotiation. But if you have a bigger deposit, many banks may be willing to lend you up to 9 times your income!

This means if you are looking to buy a home, there are two factors here. There’s the amount of debt that you’re taking on and then your income. If you can increase your salary by changing jobs, adding a side gig, or even picking up some extra shifts, you can bump up your income, which will then reduce the ratio.

The other way to change your debt-to-income ratio is to get rid of some of the debt you’re carrying. If you have a car loan or if you have credit card debt, paying those off before you apply for a loan means that your overall debt-to-income ratio will be lower.

There are many lenders to choose from out there. Some lenders will consider a DTI of up to 7, and some won’t even look at the debt-to-income ratio—they just don’t care. Working with an expert mortgage broker will help you get the right lender.

Read more: Maximise Your Borrowing Power

10. Under 12 Months In A Job

Lots of banks will want you to be in your current job for at least 6-12 months to be able to borrow with less than a 20% deposit.

In other words, if you are borrowing more than 80% of the property value (with lenders mortgage insurance), your loan will be declined if you have been in your job for less than 12 months.

Another common issue we see is people changing jobs in the middle of a home loan application, and that may negatively affect your home loan application.

Changing jobs in the middle of a home loan application

This is a big one to keep in mind, especially if you’re pre-approved because changing jobs can drastically change the application. You can have a pre-approval today based on the job that you’ve had for two years, then you might have a month off, start a new job, find a home to buy, and the bank says no, we’re not going to accept that because it doesn’t meet our policy.

Now, it’s a lot easier if you’re going to a full-time or a part-time role. Some lenders will consider you if you have industry experience for the last 2 years, especially if there is no probationary period in the new role you are changing to. In some cases, lenders may be a little bit lenient and just look at 1 payslip in your new role.

It is good to speak with your mortgage broker if you are changing jobs, especially if you’re changing to a casual position. Currently, the banks want to see 3-6 months history in any casual position.

So, it’s something to be cognitively aware of if you want to buy a property soon. Talk to your mortgage broker before you make any changes to ensure it won’t impact your ability to borrow.

At Hunter Galloway, we work with some lenders that will lend to you even if you have just started a new job.

Read More: Can You Get A Loan With A Casual Job?

11. Being Self-Employed

In many cases, the banks will decline your loan if you have been self-employed for under 2 years. The documentation required for self-employed home loans can sometimes be complex. For example, the lenders may need a letter from your accountant to confirm the business is trading profitably.

Some lenders go as far as tracking industry data for your business. For example, if you own a coffee shop, they may look at other applicants who are coffee shop owners to see how they are doing. If a lot of people in your industry are defaulting, and this has risen over the past few years, the lender may simply decline your loan.

There are lots of Mortgage Brokers (and banks) who are generalists and find self-employed applications too hard.

We are self-employed loan experts and work with several lenders that will consider home loan applications with people who have been self-employed for only 12 months. We have a team of credit experts who will help you find a lender that will work with you.

Read More: Self-Employed Finance Options

12. Additional Income

All the banks assess income in different ways. Some lenders will allow you to use 80% of bonus income, provided you’ve got 2 years’ history in the same role, whilst others will only use 60% of this income. The same goes for casual employment – some lenders need to see a 6 months’ history, whilst others want to see a 12 months’ history. Again, some lenders only take into consideration 48 weeks of the year as opposed to 52. This is also the case with overtime and commission. Each bank has different criteria for how much they’ll lend and take.

Not being able to use this additional income could drastically reduce the amount of money you can borrow. Sometimes, your loan can get declined because the bank is not considering your additional income.

If you have additional income on top of your base salary, it makes sense to speak with a broker to find ways to maximise your borrowing potential.

13. Buying A 'Difficult' Property

Previously, banks used to view things like having a helipad as a unique property. Unfortunately, these days, banks are even more particular about what type of properties they will lend on.

Some banks restrict lending for units, and others will restrict you based on bushfires or flooding.

In other cases, some banks will be okay with lending on apartments but have restrictions based on the following:

- The suburb or postcode where the unit is located, sometimes with restrictions based on high density or inner-city locations.

- How many floors the block of apartments has, sometimes with restrictions when it is higher than 4 stories.

- The total floor area inside the apartment, with restrictions if it is less than 40 square metres.

- If the bank already has too much lending in the building you want to buy in.

Case Study: Postcode Restrictions

Sarah has just found a nice house. Usually, lenders have postcode restrictions on strata titles such as townhouses or units in CBD locations. But Sarah thought she was safe because she had found a standalone house in Redbank Plains, which is Southwest of Brisbane. Sarah also qualified for the First Home Guarantee Scheme, which means she can put in as little as a 5% deposit.

But, the lender she went to has a postcode restriction on Redbank Plains. The lender was against everything in that postcode. It didn’t matter if it was a house, townhouse or unit – any property in that area had to have a minimum of 10% deposit. So even though the first Home loan deposit scheme meant Sarah could potentially put in a 5% deposit, this bank said no, we’re not going to accept that property. You need at least a 10% deposit if you are going to buy in Redbank Plains.

Luckily for Sarah, she managed to find a lender who had no postcode restrictions in that area.

Regardless of these limitations, you can still get your loan approved by going with the bank that is happy with that type of property. It’s worth working with a mortgage broker here to reduce your chances of being knocked back for a postcode or development register issue. This is because banks provide mortgage brokers with information upfront so they can check before you apply.

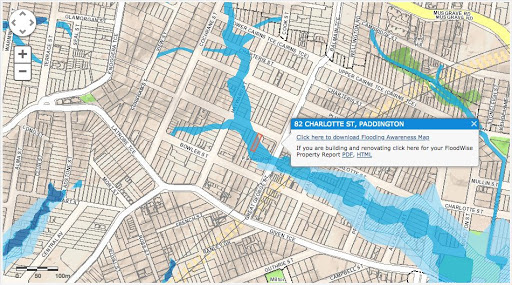

Read More: How to Flood Check in Brisbane using FloodWise Property Report.

14. Bad Credit History

A bad credit history in the eyes of the banks involves small defaults, bankruptcies and judgements on your credit file. Defaults on your credit file as small as $100 can sometimes cause the bank to reject or decline your home loan.

If you haven’t seen your credit file, you can either get in touch with us to get a copy or check out Equifax’s website to request a copy.

You should aim to have your credit score over 650 because, as we’ve said before, the banks do automatic assessments in the background. When you make an application, the algorithm will automatically spit out a yes or no. If your credit score is low, you could get automatically declined.

The banks have also started to get 2-year account payment histories from credit providers, e.g., credit cards, personal loans or car loans. This is now live across Australia, and all credit providers do this. So, for example, if you’re over 15 days overdue on a payment, it will leave a mark for the next 2 years on your credit file.

A missed payment is a red flag for some banks, especially with the more conservative banks. With some lenders, if you’ve got more than 1 missed repayment over the last 6 months, it’s just a straight-up no.

Before making an application, make sure your credit is okay and you don’t have any mishaps.

Case Study 1 - Missed Phone Repayment.

For example, we’ve recently had a first home buyer who had a small phone bill sent to their old address. This first homeowner never received the bill and wasn’t notified of it being overdue because all the mail was going to the wrong address.

As a result, the phone company put a default on their credit file for the amount owing, and the first homeowner didn’t become aware of this until they tried to apply for finance through their bank and got knocked back! Fortunately, they came to us, and we were able to help them navigate around it and find a lender that would let them buy their dream home.

Case Study 2: Credit Card Not Closed By Bank

We have a client, let’s call him James, who closed out a credit card a year or two ago. He sent a message to the bank and ripped up the card, but the bank didn’t action the closure. Instead, the bank charged a $10 monthly fee, compounding over 3 months. It showed that James was 90 days late on his repayments. This ‘default’ showed up permanently on his credit file.

We had to go back and debate it with the provider. It was a whole muck around, but we managed to fix it. However, the best thing to do is avoid it in the first place by diligently checking your credit score and keeping your credit file clean.

Having a black mark on your credit file doesn’t necessarily mean it’s the end of the world. We can help you apply with the right lender for your situation to ensure your loan is approved. Speak with our Bad Credit Experts and call us on 1300 088 065.

Read More: Positive Credit Reporting: What It Means For Home Loans.

15. Too Many Loan Applications

The banks also regularly decline home loan applications because you may have had too many credit enquiries in the past 12 months. This is not just for home loans but applies to credit cards and personal loans. All these applications show up on your credit file.

If you are putting in a minimal deposit, too many loan applications can get your loan declined. This is because the lenders mortgage insurer can see these applications and will ask many questions because they will now be suspicious. Remember, when you have minimal deposit, your loan needs to be approved by the bank AND the lenders mortgage insurer…

So be careful; making a lot of applications can reduce your credit score or flag the other banks that are assessing your application. In other words, if you have had more than 2 or 3 enquiries in the last 6 months, the banks could give you a bad credit score and reject your home loan.

Fortunately, some banks and lenders will consider your application provided there are fair reasons for the credit enquiries.

Our team regularly deals with these non-credit scoring lenders and can help you find a deal that works for you.

Read More: 21 Easy Tips To Find The Best Mortgage Broker In Brisbane

Bonus: How Credit Limits Affect Your Borrowing Capacity.

The easiest way to think about credit limits and borrowing capacity is that every $1,000 in credit limit you have reduces your ability to borrow by about $7,000. So if you have a credit card with a limit of $10,000, it is reducing your borrowing power by $70,000!

Now, even if you pay off your credit card every month, the bank will still include this as a liability. This is because, theoretically, you can max out this $10,000 credit card, and then you will have a minimum ongoing commitment to pay off that credit card, which is usually 3% of the balance each month.

Reducing your credit card limit is one of the easiest ways to increase your borrowing power. The good thing with credit card limits, too, is, in a lot of cases with a lot of banks, you don’t have to go out and rip it up today. If you’re getting a pre-approval, you can make it a condition of the pre-approval. So, if you decide to use the maximum amount you have been pre-approved for, you can close down your credit card, but if you find a cheaper house, you can leave the credit card.

The best thing to do is to check out with your mortgage broker to see if they make an impact. If they do, you can manage it, control it, and fix it up today so that it won’t be a problem tomorrow.

Bonus: What To Do If Your Home Loan Is Declined?

Don’t worry; these days, it is more common than not for a bank to decline your home loan application.

Did you know that almost 40% of applications were rejected in previous years??

The first thing you can do is speak with an Expert Mortgage Broker to discuss your situation and options. They will take the time to understand why your home loan was declined and find other banks and lenders that will look at your situation fairly.

Here are a few other things you can do if your home loan application is declined.

- Ask the lender for an explanation and try to rectify any issues that caused the loan to be declined.

- Check your credit report and ensure no errors or issues may have impacted the loan application.

- Consider applying with a different lender or seeking out alternative lending options.

- Work on improving your financial situation, such as paying off debt or increasing your income, before reapplying for a home loan.

Call us on 1300 088 065 or complete a free assessment to speak with one of our expert mortgage brokers.

Next Steps And Getting Your Home Loan Approved

Has the bank rejected your loan, or are you not sure if the bank will approve your loan?

Our team at Hunter Galloway is here to help you buy a home in Australia. Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Start again

Start again