NOTE: We want to deliver an exceptional experience for our customers, so we are only able to assist a limited number of people at a time.

Our construction loan team is currently at maximum capacity, so we are unable to accept construction loans at this time.

New applications for the HomeBuilder Grant closed at midnight on 14 April 2021. The information below is for reference only.

This is a complete guide to the $25,000 HomeBuilder Grant. In this guide, you’ll learn the following:

- If you will qualify for the HomeBuilder Grant

- The exact criteria you need to meet to receive $25,000.

- If permanent residents can qualify for the HomeBuilder grant.

- Lots of advanced tips, strategies and common questions.

While the HomeBuilder Grant may have closed, the team at Hunter Galloway – Mortgage Broker Brisbane is here to help with other grants and schemes to help you buy your first home. Contact us for a free assessment.

Let’s get started.

Table of Contents

What is the HomeBuilder Grant?

The homeBuilder is a tax-free government grant of $25,000 payable to eligible homeowners that either build a new home or substantially renovate an existing home… Eligible homeowners need to build a new home valued under $750,000 or spend between $150,000 to $750,000 on renovations of a property valued up to $1.50M.

The HomeBuilder grant is only available on building contracts signed between 4 June 2020-31 December 2020 and contracts signed between 1 January 2021-31 March 2021. Construction must begin within 18 months of the contract date.

Do I qualify for the Scheme?

The HomeBuilder scheme does have several qualifying criteria, including the type of property, your income and who you use as the builder.

To be eligible for the HomeBuilder grant, you must:

- Be aged 18 years and older.

- Be earning below an income cap. If you are applying for the grant as an individual, your ‘2018-2019 tax return or later’ must be below $125,000.If you are applying as a couple, the combined income on ‘your 2018-2019 tax return or later’ must be below $200,000.

- Have signed a building contract after 4 June 2020 and before 31 December for the $25,000 grant. The contract should be through a licensed or registered builder, so you cannot be an owner builder or use a contract from earlier in the year even if construction hasn’t started yet.

- Have signed a building contract on or after 1 January 2021 and before 31 March 2021 for the $15,000 grant. This contract should also be through a licensed builder.

- Be building a new property that you will live in as your home, where the total value of the property (house and land) is not more than $750,000. So you cannot use HomeBuilder on an investment property.

- Be buying an off-the-plan apartment or townhouse that you have signed a contract to buy on or after 4 June 2020 and on or before 31 December 2020, and construction needs to start on or after 4 June 2020 (and no later than 18 months after the contract is signed). So if you want to buy an off-the-plan property and the construction started before 4 June 2020 – even if you signed the contract after 4 June, you would not be eligible.

- Substantially renovating the existing home that you live in and spending between $150,000 and $750,000 on a renovation contract where the value of your home (house and land) is not more than $1,500,000 pre-renovation. The renovations need to “improve the accessibility, livability and safety” of your home and cannot be used to build things outside your home like a swimming pool, tennis court or sheds.

- Begin construction of your new home or renovations within 18 months of the building contract date. So if the contract is dated 1 April 2021, your builder needs to have started construction on or before 1 December 2022.

- Own or be building a property in your individual name and not as a company or trust. If more than one person is listed on the title, they must jointly apply for the grant as a couple.

- Be an Australian Citizen. Unfortunately, the Scheme is unavailable to non-residents, permanent residents or New Zealand Citizens.

Do I have to be a first home buyer to qualify for HomeBuilder?

No, you don’t need to be a first home buyer to get the $25,000 HomeBuilder grant provided you meet the eligibility criteria above. You do, however, need to be living in the property for it to meet the criteria, so you won’t qualify if the funds are for an investment property.

Gross or net income?

The income cap is similar to the First Home Loan Guarantee Scheme, so your income as an individual needs to be under $125,000 per year and as a couple, your combined income needs to be under $200,000.

- The income limit is based on your gross income, before tax and excluding superannuation.

The easiest way to check your income is to download your 2020 Notice of Assessment, which shows your taxable income for the 2019-2020 financial year.

The government has since updated the HomeBuilder Fact Sheet confirming that: Taxable income is shown on your notice of assessment. The notice of assessment is issued by the Australian Taxation Office once your tax return for an income year is processed, and this can be used to demonstrate your taxable income.

Note: Taxable income is your gross income less allowable deductions and represents the amount of income you pay tax on. You can find more information on taxable income by clicking here.

Which year will the income eligibility be based on?

The government said the income cap will be based on your individual’ 2018-19 tax return or later’.

At this stage, it is unclear if you applied for the HomeBuilder Grant from 1 July 2020 if they will allow you to use your 2018-19 income or if they will require the 2019-20 income.

The eligibility criteria say that it is based on the ‘2018-19 tax return or later ‘, implying the most recent financial year. But the case studies provided by the government show examples of people applying for the grant post 1 July 2020 with income being verified from 2018-19 returns.

The First Home Loan Guarantee scheme, which uses the same income eligibility cap states that:

- Singles – your taxable income for the previous financial year must not be more than $125,000.

- Couples – your combined taxable income for the previous financial year must not be more than $200,000

The First Home Loan Deposit scheme explicitly says:

- For all First Home Loan Deposit Scheme places reserved up to 30 June 2020, you will need to provide a copy of your Notice of Assessment from the Australian Taxation Office for the 2018-19 financial year.

- For all First Home Loan Deposit scheme places reserved from 1 July 2022 to 30 June 2023, you will need to provide a copy of your Notice of Assessment from the Australian Taxation Office for the 2021-2022 financial year.

As we do not have the application form and official paperwork for HomeBuilder, we cannot confirm how the government will test your income if you applied for HomeBuilder after 1 July 2020.

In other words, we do not know if the government will base your income on the 2018-19 tax return or use the 2019-20 tax return, as this would be considered the previous financial year from 1 July 2020 onwards.

However, if you have a change of situation – i.e. income change – you need to be aware that the HomeBuilder FAQ states:

If your circumstances change after you have applied for HomeBuilder but have not yet received the payment, and no longer meet the eligibility criteria, you will need to notify your State or Territory revenue office immediately.

Do Permanent Residents or Indefinite Visa Holders qualify for the HomeBuilder?

Again they have used similar criteria to the First Home Loan Deposit Scheme, which is only available to Australian Citizens.

So you will not qualify if you are a:

- Permanent Resident

- New Zealand Citizen

- Indefinite Stay Visa

While the First Home Owners Grant is available to permanent residents and New Zealand citizens, unfortunately, the HomeBuilder will not be available to you if you aren’t an Australian citizen.

Read More: Can NZ Citizens buy property in Australia?

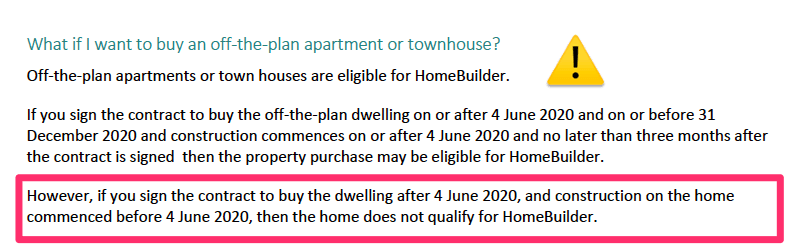

Can I get HomeBuilder on a brand new off-the-plan apartment or townhouse?

This was something that was up for interpretation when the HomeBuilder was first released, as it said that the $25,000 grant would apply to “All dwelling types (house, apartment, house and land package, off-the-plan, etc.).”

The government clarified this.

If:

- You have found a newly completed property you want to buy.

- That has never been lived in before.

Then:

The $25k HomeBuilder grant may only apply if:

- You sign the contract to buy the off-the-plan dwelling between 4 June 2020 and 31 March 2021

- Construction commences on or after 4 June 2020 and no later than 18 months after the contract is signed.

- And it will not apply if construction has commenced on the property before 4 June 2020.

So if the construction of the property started before 4 June 2020, HomeBuilder will not apply.

But if you are a first home buyer and buying a new property, you may still be eligible for your state’s first home buyers grant.

What won’t HomeBuilder cover?

If that is a bit too much info on what HomeBuilder will cover, you might be better off looking at the exclusions from HomeBuilder.

In this section, we’ll show you all the exclusions, i.e. what you cannot use HomeBuilder for and how to make the Scheme work for your situation.

HomeBuilder Exclusions

HomeBuilder is only available for building contracts, so it is not available if you are:

- Building or renovating an investment property.

- Building a new home that has a combined land and home value of over $750,000.

- Building a granny flat.

- An owner builder, or constructing or renovating through an unlicensed or unregistered builder.

- A permanent resident, New Zealand Citizen or visa holder.

- Building something not connected to your home, for example, a swimming pool, tennis court, outdoor spa, sauna, shed, garage or granny flat.

The government specifically mentioned Granny Flats in their most recent FAQ, stating that.

Standalone granny flats are not eligible for HomeBuilder. For more information, please refer to the FAQ ‘What renovations are eligible?’.

What if you already own land but haven’t signed a build contract?

You will be eligible if:

- You own a property (house and land) and knock the house down to rebuild – this will be counted as a substantial renovation and, therefore, subject to the renovation price range of $150,000 to $750,000, provided the total value (house and land) of the property does not exceed $1.5 million pre-renovation;

- You own vacant land before 4 June 2020 and then build. The total value of the land and new build cannot exceed $750,000; or

- If you buy the land after announcement and then build. The total value of the land and build cannot exceed $750,000.

Renovation Exclusions

If you are renovating a property, you need the work to be completed by a registered or licensed builder. So you will not be able to get a friend or employ tradespeople to complete the renovations.

As we covered above, Homebuilder needs the renovations to “improve accessibility, livability and safety of the property”. This excludes building a tennis court, pool or shed. You also need to be using a currently registered builder, and you can confirm this by providing their building license details when you apply for HomeBuilder. The government specifically says:

Renovations must be completed by a licensed or registered builder. In addition, any building or renovation contract entered into must be at arm’s length. This means the contract must be made by two parties freely and independently of each other. The terms of the contract should be commercially reasonable, and the contract price should not be inflated compared to the fair market place.

The way they will determine if the contract price is reasonable is by requesting this information from the builder:

The registered or licensed builder (depending on the State or Territory) must demonstrate that the contract price for the new build or substantial renovation is no more than a comparable product (measured by quality, location and size) as at 1 July 2019, if requested by the purchaser.

Read More: Complete Guide to Renovation Loans

How will they determine the valuation of your property?

This is another point that has been a grey area. The government confirmed how they will assess the $1.50M value for substantial renovations:

The evidence to demonstrate the value of your property is a matter for determination by each State and Territory. States and Territories may consider evidence such as a recent contract of sale for the property, a rates notice that identifies the Capital Improved Value, or a bank or independent valuation. Further information will be available through your State or Territory.

Can you Build a Duplex and claim HomeBuilder?

While HomeBuilder will apply to all dwelling types, if you are building a duplex, you will only be able to claim one of the properties as your principal place of residence, making the other property an investment and therefore ineligible for the HomeBuilder Grant.

“Owner-builders and those seeking to build a new home or renovate an investment property are ineligible for HomeBuilder.”

Read More: Building a Home in Brisbane

Using HomeBuilder towards your deposit

Now it’s time to cover a SUPER exciting part of the HomeBuilder scheme—using it towards your deposit.

HomeBuilder could help reduce your Lenders Mortgage Insurance cost by thousands—Or just help you borrow less and pay off your loan faster.

Home Deposit Basics

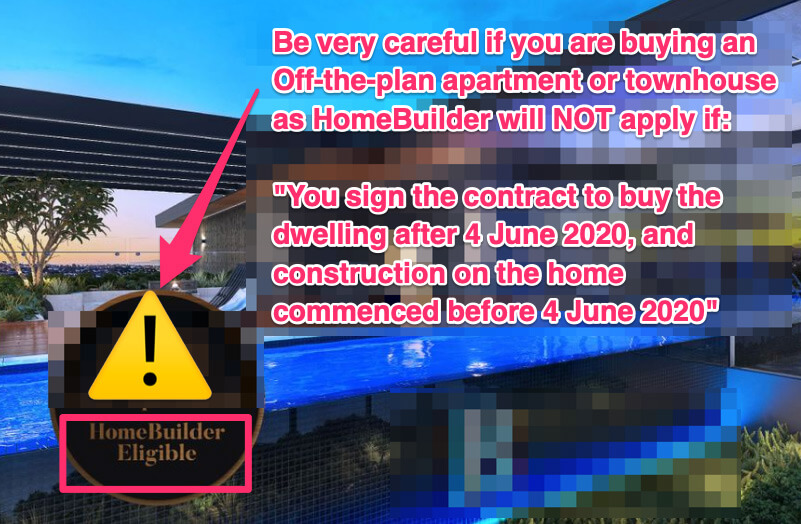

Can I use HomeBuilder as a deposit? This is the first question that home buyers ask us, and it should be straightforward to work out… but it often isn’t.

While you might have read some banks will do 95% loans, many people assume this means you only need a 5% deposit, which is incorrect.

A common mistake many homebuyers make is not to factor in many other costs. Once you factor in these costs, you will realise you actually need closer to an 8% deposit.

If you are buying your second home, you will also need stamp duty on top of this, so the costs might be over 10% minimum of the purchase price.

Read More: Deposit Calculator

Bank Deposit Criteria

Most banks will consider HomeBuilder in the same light as the First Home Owners Grant, and it will be viewed as non-genuine savings.

Unlike the First Home Owners Grant, which can be factored as part of your bank deposit, the banks will not factor HomeBuilder as part of your savings deposit when assessing your loan application because, according to the FAQ Sheet, this is how the grant will be paid:

- New builds: grants will be paid after the foundations have been laid and the first progress payment has been made to your builder

- Substantial renovations: grants will be paid after construction has commenced and at least $150,000 of the contract price has been paid in respect of the renovation.

- Off-the-plan / new home purchases: grants will be paid after the applicant(s) name is registered on the title.

The grant will be paid after work commences, which means you will not be able to include this 25k in your initial deposit.

However, the good news is that the grant will be paid directly into your account once approved, as they state:

The relevant State or Territory revenue office will distribute the $25,000 grant directly to the applicant.

The bad news is that it may be a little while down the track and won’t help reduce your LMI costs.

No deposit loans with HomeBuilder

We have to say, this was probably the most exciting prospect for many first home buyers out there.

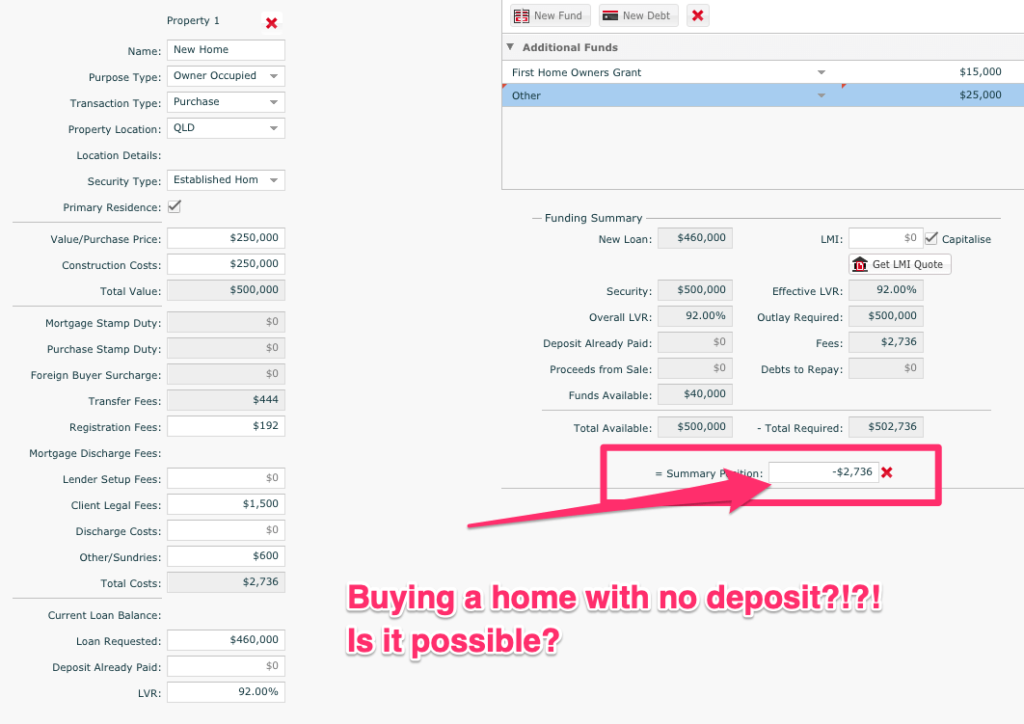

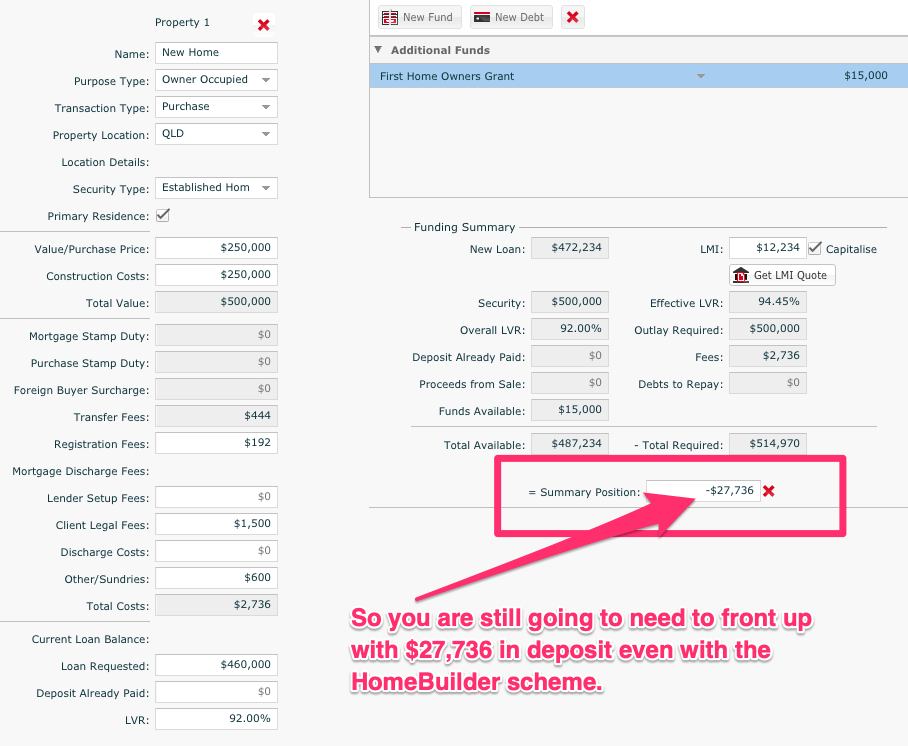

You could get a three-way boost hypothetically. For example, on a $500,000 house and land package in Queensland, you could get $52,234 in benefits from the government!

This could look like this:

- First Home Owners Grant—$15,000

- HomeBuilder Scheme —$25,000

- First Home Loan Guarantee Scheme ($12,235 saving in LMI)

(PLUS, you could have been using the First Home Super Saver Scheme and have another $30,000 deposit but let’s not go there)

On a $500,000 house and land package, you could:

- Borrow $460,000

- Put in $15,000 first home owners grant

- Get $25,000

You’d only need to put in $2,736 in deposit!!

This is the dream, but what is the reality?

As stated above, the grant will only be paid once work has already begun on your build or renovation.

This being the case, the banks will want to see you have at least $27,736 in savings to cover your deposit.

And then, provided you meet all the requirements of HomeBuilder, the government will pay you back your $25,000 grant in the future, which you can use to pay down your loan!

Read More: Deposit Calculator, learn how much deposit you need today

First Home Buyers Grant, First Home Loan Guarantee Scheme & HomeBuilder

When it comes to government grants, one is good, but three is better…

That said…

Is it possible to use both the First Home Owners Grant and HomeBuilder scheme together? And if you can, are you also able to also use the First Home Loan Deposit scheme?

In this section, we’ll take you through the different schemes for first homeowners state by state.

Using Multiple Grants

Provided you meet the criteria of both schemes, you can apply for the First Home Owners Grant in your state and also access the HomeBuilder Scheme.

First Home Buyer Schemes – State by State

Let’s break down the different first home owners grants, state by state, remembering that these first home owners grants are only available on newly built properties that have never been lived in before.

- Queensland: $40,000 for first home buyers

- First Home Owners Grant in QLD: $15,000

- HomeBuilder Scheme in QLD: $25,000

- Restrictions: Only available on new homes valued up to $750,000

- Read More: Check out our complete guide to the First Home Owners Grant 2023.

- New South Wales: $35,000 for first home buyers

- First Home Owners Grant in NSW: $10,000

- HomeBuilder Scheme in NSW: $25,000

- Restrictions: While the stamp duty exemptions are on houses valued up to $800,000, the first home owners grant + HomeBuilder scheme will limit your new build to a land and build value of $750,000.

- Read More: Check out the NSW Office of State Revenue’s First Home Owner Grant (New Home) page here.

- Victoria: $45,000 for first home buyers

- South Australia: $40,000 for first home buyers

- First Home Owners Grant in SA: $15,000

- HomeBuilder Scheme in SA: $25,000

- Restrictions: Only available on new homes valued up to $750,000

- Read More: Check out SA’s Office of State Revenue’s first home owner grant page here.

- Tasmania: $45,000 for first home buyers

- First Home Owners Grant in TAS: Up to $30,000

- HomeBuilder Scheme in TAS: $25,000

- Restrictions: Only available on new homes valued up to $750,000.

- Read More: Check out Tasmania’s Office of State Revenue’s first home owner grant page here.

- ACT: $25,000 for first home buyers

- First Home Owners Grant in ACT: None

- HomeBuilder Scheme in ACT: $25,000

- Restrictions: Only available on new homes valued up to $750,000

- Read More: Check out ACT Office of State Revenue’s first home owner grant page here.

- Western Australia: $35,000 for first home buyers

- First Home Owners Grant in WA: $10,000

- HomeBuilder Scheme in WA: $25,000

- Restrictions: Only available on new homes valued up to $750,000

- Read More: Check out WA’s Office of State Revenue’s first home owner grant page here.

- Northern Territory: $35,000 for first home buyers

- First Home Owners Grant in NT: $10,000

- HomeBuilder Scheme in NT: $25,000

- Restrictions: Only available on new homes valued up to $750,000

Read More: Check out NT’s Office of State Revenue’s first home owner grant page here.

Are there any states that are opting out / not offering the grant?

The HomeBuilder Grant is available in every state and territory in Australia and will be processed by your State’s Office Of State revenue.

HomeBuilder Application Process

Now it’s time for the rubber to hit the road.

- How do you actually apply for the HomeBuilder Grant?

- What is the process, and what documents will you need?

- And more importantly, at what stage will the HomeBuilder be paid during the construction?

In this section, we’ll answer all of these questions and more.

How do you actually ‘apply’ for the grant?

You will need to apply for the HomeBuilder through your local state or territory revenue office; their details are below.

The government has said that the states will backdate acceptance of HomeBuilder applications to 4 June 2020 once the official agreement has been signed.

State | Website |

Queensland | https://www.qld.gov.au/housing/buying-owning-home/financial-help-concessions/homebuilder/apply |

New South Wales | |

Victoria | |

Western Australia | https://www.wa.gov.au/service/community-services/grants-and-subsidies/australian-government-homebuilder-grant |

South Australia | |

ACT | https://www.revenue.act.gov.au/covid-19-assistance/homebuilder-grant |

Northern Territory | https://treasury.nt.gov.au/dtf/territory-revenue-office/homebuilder-grant |

Tasmania | https://www.treasury.tas.gov.au/about-us/tasmanian-homebuilder-grant |

When and at what stage can the grant be applied during the construction, and when do we finally get it?

As the government states:

Timing of payment for the HomeBuilder Grant depends on whether your application relates to a new build, substantial renovation or off-the plan / new home purchase:

- New builds: grants will be paid after the foundations have been laid and the first progress payment has been made to your builder.

- Substantial renovations: grants will be paid after construction has commenced and at least $150,000 of the contract price has been paid in respect of the renovation.

- Off-the-plan / new home purchases: grants will be paid after the applicant(s) name is registered on the title.

In Tasmania, the timing of the grant payment may be different in certain circumstances and you should refer to the State Revenue Office of Tasmania website for further information.

The government hasn’t yet confirmed when this will be paid, but it does say the HomeBuilder grant will be paid directly to the applicant – i.e. you!

This most likely means that it will get paid to you after the construction has started, and with it not being paid to the bank, it’s unlikely that the $25,000 grant will be usable towards your deposit.

The government has confirmed that the HomeBuilder Grant will not be taxed, in line with the First Home Owners Grants.

What documents do you need to apply for HomeBuilder?

Your local office of state revenue will have its own checklist, but at a minimum, the government has said you will need to provide the following:

- Proof of identity, photo ID

- A copy of the contract, dated and signed by you and the nominated registered or licensed builder;

- A copy of the builder’s registration or licence (depending on the state you live in);

- A copy of your 2018-19 tax return (or later) to demonstrate your eligibility against the income cap; and

- Documents such as council approvals, building contracts or occupation certificates and evidence of land value.

Advanced HomeBuilder Tips

Now that you’ve mastered the basics of HomeBuilder, it’s time to cover some of the advanced stuff.

Specifically, we will reveal strategies that you could implement right away.

So without further ado, let’s dive right into the tips.

Buying With a Partner That Isn’t a Citizen

We’ve been asked variations of this question lots of times in the past few days:

- Would we still get the grant if the mortgage is in joint names (one applicant PR & one applicant citizen) & the title is in the citizen applicant’s name?

- But what if my wife is a citizen and I’m still on p.r? Am I qualified for that?

- I am a citizen, and my wife is not. Would I still qualify for the homebuilder grant?

The government’s response to this is:

If two people are listed on the title as registered proprietors they must apply for HomeBuilder as a couple, and both applicants must meet the eligibility criteria of the program. The HomeBuilder program is only open to Australian citizens.

Chat with our Mortgage Brokers and see how we can help.

Recently Changed Jobs to a New Company

Just changed jobs to a new company. Still full-time employed with a good income in a similar industry. How long would I have to have been in a new job for a bank to give me a loan?

Chat with our Mortgage Brokers, as we have several banks that only need 1 pay slip from your new job to qualify for a home loan. You can even be on a probation period.

Next steps and getting your home loan.

Our team at Hunter Galloway is here to help you buy a home in Brisbane. Unlike other mortgage brokers who are just one person operations, we have an entire team of experts dedicated to help make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Resources and further reading

- Building a Home.

- How does construction finance work – Complete guide

- Renovation Loans

- Official government website for HomeBuilder –

- HomeBuilder Fact Sheet

- HomeBuilder FAQ

NOTE: This article is general in nature and not to be taken as advice. Please seek legal advice before applying for the Home Builder Grant, and if you want to 100% confirm you qualify, please contact your local Office of State Revenue.

Start again

Start again