Buying your first home is a huge achievement – but carrying a mortgage for 30 years can feel like a financial weight on your shoulders. For many Australian first-home buyers (often young professionals and families), the goal is to become debt-free as soon as possible. Paying off your mortgage early can save you tens of thousands in interest and bring peace of mind and financial freedom years sooner. In this comprehensive guide, we’ll walk through the following:

- Proven strategies to pay off your mortgage completely in a short time

- Financial considerations and risks to weigh

- Important Australian regulations and schemes to know about

- Common mistakes to avoid

- Real-life case studies of Aussies who crushed their mortgages early.

By the end, you’ll have an actionable roadmap to become mortgage-free – and confidence that it can be done with (or without) the help of a mortgage broker in Brisbane, even if you’re a first-home owner with a modest income. Let’s dive in!

Introduction

Paying off your mortgage faster means less of your hard-earned pay is eaten up by the loan, and you can redirect money to other goals such as travel – you won’t have to wait until you are old and can no longer enjoy the trips. You can also channel the money towards investments or your family’s needs much earlier in life.

However, there are also myths and misconceptions around paying off a home loan early. Some people think ‘you must be wealthy to pay off a mortgage fast’ or that ‘there’s no point paying it off if interest rates are low’. In reality, even modest extra payments can shave years off a loan. And while mortgage rates might seem low at times, they won’t always stay that way – Australia’s average mortgage interest rate hit about 6.1% in late 2024, up from record lows near 2.6% in 2021, reminding everyone that rates can rise quickly. Another misconception is that paying off your loan will hurt your credit score or that you should ‘always invest instead’.

We’ll address all of these in detail, but suffice it to say, being debt-free is usually a solid financial win, and any short-term credit score dip from closing a loan is minor and temporary.

Why You Should Pay Off Your Mortgage Completely.

Paying off your mortgage ahead of schedule is a significant financial milestone for many Australian first-home buyers. Beyond the obvious benefit of owning your home outright, accelerating your mortgage repayments offers numerous advantages. Here are compelling reasons to consider paying off your mortgage completely:

1. You save THOUSANDS on interest

Reducing your loan term decreases the total interest paid over the life of the mortgage. For example, paying off a $600,000 loan with a 6.1% interest rate over 30 years results in approximately $708,046 in interest. By shortening the term to 15 years, the interest drops to around $311,725, saving a jaw-dropping $396,321!

2. More Financial Security

Getting rid of mortgage debt reduces your monthly financial obligations, providing greater flexibility and security. Without home loan repayments, you have more disposable income to allocate towards savings, investments, or other financial goals.

3. Build Home Equity Faster

Paying down your mortgage faster builds home equity more rapidly. This equity can be leveraged for future financial needs, such as paying for renovations, buying more properties, or refinancing to get a better deal.

4. Reduced Financial Stress

Owning your home outright can reduce the anxiety associated with debt and financial commitments. The peace of mind that comes with full ownership allows you to focus on other aspects of your life without the burden of monthly repayments.

5. You retire with no debt

Entering retirement without a mortgage reduces your living expenses, allowing your retirement savings to stretch further. This financial freedom enables a more comfortable and secure retirement.

6. Protection Against Interest Rate Fluctuations

Variable interest rates can lead to unpredictable mortgage repayments. By paying off your mortgage early, you eliminate the risk associated with rising interest rates, ensuring your financial stability.

7. No Risk Of Foreclosure

Paying off your mortgage completely means you’re not at risk of foreclosure due to missed payments. This security is particularly valuable during economic downturns or personal financial hardships.

8. Higher Borrowing Capacity

Without existing mortgage debt, your debt-to-income ratio improves, making you a more attractive candidate for future loans or credit, should the need arise.

How to Pay Off A Mortgage Faster

There are several strategies you can use (often in combination) to accelerate your home loan payoff. But it all comes down to simple principles: pay more, pay sooner, or pay less interest. All of these reduce the total time and cost of your mortgage. Below are some of the most effective tactics:

1. Make Extra Repayments (Even Small Ones)

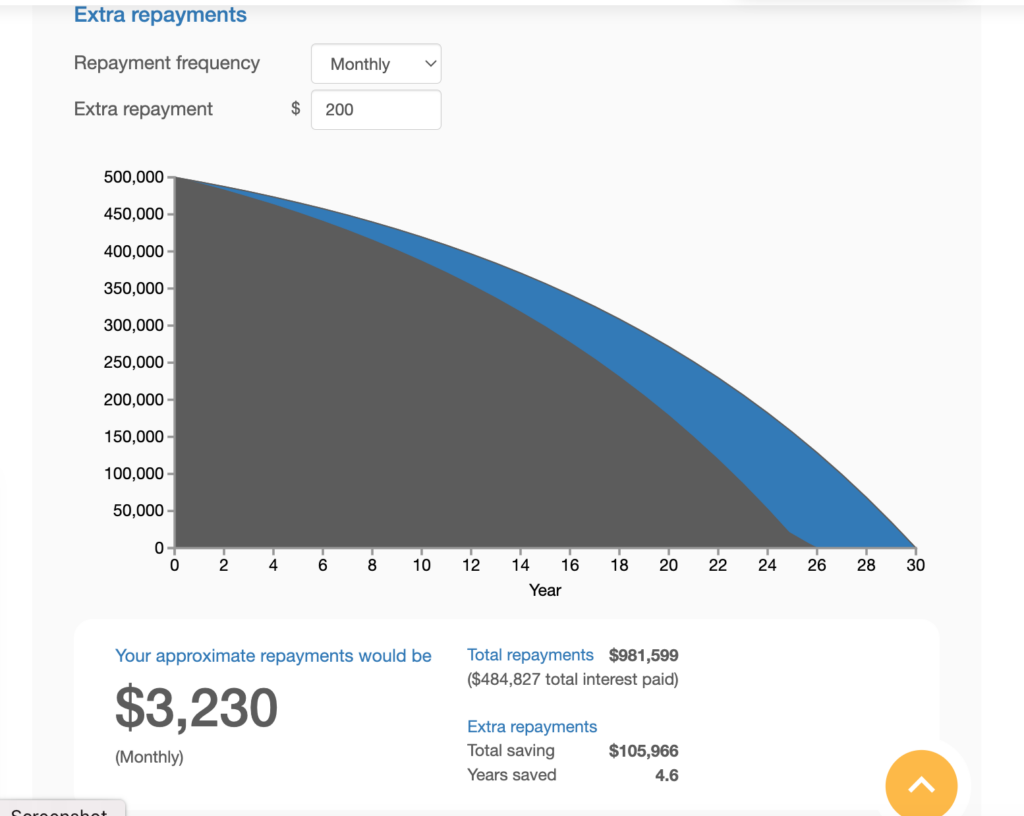

One of the simplest ways to get ahead is to pay more than the minimum required. Any extra repayment – whether it’s an extra $50 a week or a lump sum from a bonus – goes straight towards reducing your loan principal. This can cut your loan by years and save you thousands in interest. For example, according to our extra repayments calculator, adding just $200 extra per month on a $500,000 loan can save more than $100,000 in interest over the life of the loan! That’s a huge saving for a relatively small monthly sacrifice.

Consider directing windfalls into your mortgage: tax refunds, work bonuses, inheritance, or proceeds from selling an old car or items. As one homeowner who paid off her loan in 12 years shared, “I always paid more than the mortgage payment and if any extra money came my way… I put it on the mortgage, so it was reducing quickly.” The earlier in your loan, you make extra payments, the more interest you’ll save since most interest is charged in the early years.

Just be sure to check with your lender about any fees or limits: some loans, particularly fixed-rate mortgages, may charge an early repayment fee or cap how much extra you can pay each year without penalty. Many Australian loans, especially variable-rate ones, now have no penalties if you pay off your mortgage completely since exit fees on new home loans were banned in 2011. But always double-check your loan’s terms.

Expert Tip: Set up an automatic transfer of a small extra amount each payday toward your home loan. You’ll hardly notice, but over time, it makes a big dent in the balance. Even rounding up your payment, like paying $550 instead of $520, helps build an extra buffer. Every dollar pushed into your principal now saves you interest on that dollar for the remainder of the loan term.

2. Switch to Fortnightly (Biweekly) Repayments

Switching from monthly to fortnightly repayments is a classic hack to pay off a loan faster. Most monthly mortgages equal 12 payments per year. But if you pay half your monthly amount every two weeks, you end up making 26 half-payments a year – which adds up to 13 full monthly payments. In effect, you’ve made one extra monthly payment annually. This simple change can take several years off a 30-year loan.

For example, paying fortnightly means someone with a $500,000 loan might finish about 4 years earlier. Many Aussie lenders allow you to choose weekly or fortnightly payment frequencies at no cost. If yours doesn’t, you can achieve the same effect by manually paying extra each month equivalent to one additional payment per year.

Fortnightly payments also align well with how most people get paid, making budgeting easier. You essentially synchronise your mortgage outflows with your pay cycle, which can help avoid late payments and reduce interest compounding. Over time, that speeds up your payoff without much effort on your part.

3. Use an Offset Account

Many Australian home loans come with or allow an offset account – a powerful feature to reduce interest costs. An offset account is essentially a savings or transaction account linked to your mortgage. Any balance in that account “offsets” the loan principal for interest calculation. For example, if you owe $600,000 on your loan and have $20,000 in your offset account, the bank will only charge you interest on $580,000 that month. This means your entire $20k is working to reduce your interest while still being accessible to you if needed. By parking spare cash, salary, or savings in offset, you effectively pay your mortgage faster because more of each payment goes to the principal since the interest charge is smaller.

Offset accounts are great for first-home buyers who want to keep access to savings for emergencies, renovations, etc., while reducing mortgage interest. If you maintain a decent balance in offset over time, it can shave years off the loan. One couple who paid off their mortgage in 4 years credited using an offset account as one of the key strategies they used. Do note: some banks charge a monthly fee or require a package for an offset account, so ensure the benefit outweighs the cost. Generally, if you keep only a very low balance (say under $5-10k) in offset, the savings might be negligible. In that case, you might focus on direct extra repayments or other strategies. But if you can build up your offset through disciplined saving or depositing all income there, it’s a flexible way to cut interest while keeping funds available.

Redraw vs. Offset

Often talked about together, redraw facilities are slightly different. A redraw allows you to pull out any extra repayments you’ve made on your loan if you need the money back. However, it differs from an offset because an offset is a separate account, whereas redraw is withdrawing from the loan itself. Offset savings don’t count as loan payments, so the loan balance doesn’t formally reduce; you just pay less interest. With redraw, you actually paid down the loan and are taking out those extra funds back. Many modern loans offer both features. The main thing is to use one of them. Don’t leave spare cash idle in a 0.5% savings account while paying 6% on your mortgage! Put your money to work against the mortgage either via offset or extra payments with redraw capability.

4. Refinance to a Lower Interest Rate

Interest rate is one of the biggest factors determining how long your mortgage drags on. A lower rate means more of your payment goes to principal rather than interest. Refinancing involves switching your loan to a new lender or negotiating with your current lender to get a better deal. In Australia’s competitive home loan market, finding a lower rate is often possible, especially if it’s been a couple of years since you took the loan. New customers often get enticing rates, while existing borrowers might pay higher than necessary. This higher interest is commonly referred to as loyalty tax. By refinancing from, say, a 6.0% loan down to 5.5%, you could save thousands per year in interest – money that effectively speeds up your payoff if you keep repayments the same or higher.

Start by researching and comparing rates on similar loan products: look at comparison rates, not just advertised rates, which may exclude fees. If you find a significantly better rate, you can ask your current bank to match it or give you a discount – they often will agree to retain your business. If they won’t, consider switching to a new lender.

Expert home loan tip: Weigh the costs of refinancing against the savings. Typical costs can include a loan application fee for the new loan and a discharge fee for the old loan, usually modest, around $300. If you are on a fixed rate, a break cost may apply, which may be high if rates have fallen since you fixed. Also, check if you’ll lose any features, such as offset, that you value.

Refinancing can also mean resetting your loan term (sometimes back to 30 years). To truly pay off faster, try to keep your payments at the same dollar amount as before, rather than lower them with the new lower minimum. That way, all the interest savings will translate into principal reduction. Lastly, refinancing isn’t a one-time option. You can periodically review your mortgage and see if the market offers something better. Just avoid doing it too frequently, as multiple credit inquiries in a short time can impact your credit score.

5. Consider Debt Consolidation

For first-home buyers, this strategy can be a bit of a double-edged sword, but it’s worth mentioning. If you have other high-interest debts like credit cards, personal loans, or car loans, consolidating them into your home loan through a refinance can reduce your overall interest costs, simplify your finances and help you pay off your mortgage completely. Home loans typically have much lower interest rates than credit cards or personal loans – perhaps 5–6% vs 15–20%.Rolling those debts into your mortgage could cut your interest burden each month. It also means you have just one repayment instead of many and only one interest rate. This can lower your total monthly outgoings and reduce the risk of missing a payment on one of many debts.

Example: Suppose you’re paying $300/month on a car loan, $200 on a credit card, and $1,500 on your mortgage. If you refinance and add the car and card debt into the mortgage, your new single payment might be $1,800. If you continue paying the original total ($2,000 in this case), you’d be paying $200 above the minimum – effectively an extra repayment that helps pay off the mortgage faster. In effect, if you keep your loan repayments the same as what you were paying for all your individual debts, you could pay off your mortgage faster.”

Proceed with caution: While consolidating, do not fall into the trap of only paying the minimum on the new bigger mortgage. If you stretch short-term debts over a 30-year home loan without increasing payments, you might end up paying more interest in the long run. Also, your home loan balance will increase when you add other debts to it, and if it pushes your LVR above 80%, you could incur LMI or a higher rate. You’re also converting unsecured debts (like credit cards) into secured debt against your house – meaning if you fail to pay, your home is on the line. So, this strategy is best only if you have the discipline to keep repayments high. It can be a smart move to reduce interest costs and streamline payments, but always do the math or talk to a financial adviser/mortgage broker to ensure it’s truly beneficial for you.

6. Avoid Interest-Only Loans and Pay Principal & Interest

When the goal is to be mortgage-free, you want to chip away at the principal as much as possible. With an interest-only loan, you’re only paying the interest charges each period and not reducing the principal at all during the interest-only term. These loans are usually short-term and popular with investors or to keep repayments low initially. However, for an owner-occupier first-home buyer, interest-only loans will delay your debt-free date significantly. They cost more in the long run as these loans tend to have higher interest rates, and when they revert to principal payments, the remaining term is shorter, so required payments jump up.

ASIC’s MoneySmart bluntly advises that paying principal and interest is the best way to pay off your mortgage completely. . With each payment, you’re gradually reducing the loan balance. It might feel slow in the first few years because interest takes a big portion of each payment, but it will accelerate. Every dollar off the principal saves you interest on that dollar for all future years. Unless you have a very specific strategy and advice from a financial expert, steering clear of interest-only terms will ensure you’re always moving closer to outright ownership.

If you currently are on an interest-only loan, consider switching as soon as you can, or at least setting aside extra repayments in an offset account so that your principal is effectively reduced. The faster you transition into paying principal, the sooner you’ll pay off the mortgage.

Case Study: Tammy and John – Mortgage-Free in 4 Years

Perth couple Tammy and John bought a modest home (3-bedroom, 1-bath) in Middle Swan, WA. Their loan was $500,000 after a 20% deposit on a $625,000 house. Incredibly, they managed to pay off this mortgage in just under four years, finishing by age 27 without any windfall like lotto or inheritance. How did they do it? Their strategy was extreme, but you can glean some tips from it:

- They temporarily moved to regional WA to earn extra income. They rented out their house in Perth. The rent from tenants helped cover a chunk of the mortgage. Essentially, they combined earning more with reducing their housing costs since Rob’s company provided their accommodation.

- They made double the required payment every fortnight. If the bank asked for (say) $1,500 fortnightly, they paid $3,000. This aggressive payment schedule rapidly slashed the principal. Fortnightly payments already give you that one extra yearly payment; doubling them is like making 27 or more payments a year. This only works if you have a lot of surplus income, hence the need for high earnings and low expenses in that period.

- They lived very frugally. In other words, no luxuries, no unnecessary spending. Avocado toast has become a symbol in Australia’s housing affordability debate – Tammy and John turned that on its head by showing discipline.

- They also avoided credit cards entirely to avoid any other debt.

The result: over four years, they paid only about $23,000 in interest on the loan – versus what would normally be over $100,000 in interest over a typical 25 to 30-year loan term. To put that in perspective, on a $500,000 loan at 6.1% interest, one year’s interest alone is around $30,500. They compressed 25-30 years of payments into four, saving an enormous amount of interest.

Can everyone replicate this? No – it required them to relocate, work hard, and basically put their life on hold for a few years. However, elements of their approach can inspire others: for example, even if you can’t double payments, perhaps you can increase your repayment by a smaller factor and take on a side hustle for a few years. Or consider renting out a room or the whole home for a period to generate extra income. Tammy and John prove that with determination and sacrifice, young people can crush a mortgage fast. They also underscore the value of keeping the loan as small as possible to start – they bought a house within their means, not stretching for something extravagant.

Financial Considerations & Risks Before Paying Off Mortgage Completely

Becoming mortgage-free faster is an attractive goal, but it shouldn’t come at the expense of your overall financial health or other opportunities. First-home buyers are often balancing multiple priorities – starting families, building careers, saving for the future – so it’s important to consider the broader picture. In this section, we highlight key financial factors and potential risks to weigh when ramping up your mortgage repayments:

1. Opportunity Cost: Pay Off Mortgage or Invest Elsewhere?

Every dollar you direct to paying down your home loan is a dollar you aren’t investing in other assets like superannuation, shares, or a second property. This trade-off is known as opportunity cost. The big question many ask is: “Am I better off putting extra money into my mortgage, or investing it for potentially higher returns?” The answer depends on a few factors:

- Your mortgage interest rate vs. expected investment return: Paying off your mortgage gives a guaranteed, risk-free return equal to your interest rate. For example, if your rate is 5.5%, extra repayments earn you a 5.5% return (in the form of interest saved). It’s hard to find a surefire investment with that kind of return, especially after tax. By contrast, investing in shares or property might yield higher. Historically, the Australian stock market might return ~7-10% per year, but those returns are not guaranteed and come with risk and volatility. Some years, you could get 15% returns; other years -10%. So while the average market return could beat your mortgage rate, there’s no certainty – whereas every dollar saved in interest is yours to keep.

- Risk tolerance: As we have just mentioned, investment is riskier. Some people feel comfortable carrying a big debt while investing spare cash, hoping the math works out in their favour. Others prefer the peace of mind of paying off their mortgage completely (i.e., debt freedom). If the thought of owing money stresses you out, the psychological benefit of eliminating the mortgage might outweigh the potential extra gains from investing. On the flip side, if you’re an experienced investor with a high-risk tolerance, you might be okay with a slower mortgage payoff while your money works in the market.

- Timeline and life stage: For young first-home buyers, retirement is decades away, so investing in super or stocks has a long runway to compound. Small investments now could grow substantially over 30 years. Meanwhile, your mortgage is front-loaded with interest in the early years. A more balanced approach would be to continue contributing to super (especially if you get employer matching contributions, or tax benefits via salary sacrifice) while also making some extra mortgage payments. If you’re closer to retirement, clearing the mortgage may take priority since you want to enter retirement debt-free.

- After-tax considerations: Remember that returns on investments (like dividends and capital gains) may be taxed, whereas the “return” from paying off your home loan is tax-free (you’re just not paying interest). So, a 7% investment return might net you ~5% after tax, depending on your bracket, making it closer to break-even with your 5% mortgage cost. For investment properties, note that their mortgage interest is tax-deductible – which can complicate the pay-off-mortgage-completely question.

There’s no one-size-fits-all answer. Mathematically, if you can consistently get a higher after-tax return on investments than your mortgage interest rate, you’d end up wealthier by investing rather than paying down the loan. But real life isn’t just math – risk and peace of mind matter. Many experts suggest a balanced approach: pay off your mortgage aggressively enough to reach a comfortable equity level, but also invest in parallel high-yield opportunities). You could, for instance, put 50% of your surplus cash into extra home loan payments and 50% into an index fund or additional super contributions. Regularly review the strategy as interest rates or your circumstances change. And whichever path you lean towards, being debt-free by retirement should be a key goal – you don’t want a mortgage hanging over you when your income stops.

2. Early Repayment Fees or Restrictions

In Australia, early repayment fees on home loans have largely been curtailed by regulation, but it depends on your loan type. If you have a variable-rate loan that was taken out after July 1, 2011, you cannot be charged a punitive exit fee for paying it off early or refinancing. Lenders can still charge a modest administrative discharge fee, usually $150–$350 when you close the loan, but no hefty “deferred establishment fee” like in the past. So, for most first-home owners on variable rates, you have the flexibility to make extra payments or refinance without fear of a large penalty.

Be careful! If your loan was very recently originated, say less than 2–3 years ago, check if there’s a fixed cash-back clawback or similar – some banks give cash-back offers and might stipulate you keep the loan for a minimum period or repay the cash-back if you leave too soon.

For fixed-rate loans, it’s a different story. Fixed loans usually have break costs if you repay more than an allowed amount or refinance during the fixed period. The cost depends on how interest rates have moved since you locked your fix. If rates have fallen, the break fee can be substantial because the bank loses money on the deal. Some fixed loans allow a certain amount of extra repayments per year (e.g. up to $10,000) without fees – anything beyond that triggers a penalty.

Also, some loans (like basic “no-frills” loans) might not have formal penalties but simply won’t allow you to go into advance by more than a set amount or might not offer redraw on extra payments. It’s always good to know your loan’s features. If you find your loan is too restrictive for your prepayment goals, that’s a sign to perhaps refinance to a more flexible product.

2. Impact on Credit Score

Some borrowers worry that paying off a large debt like a mortgage could hurt their credit score. Here’s the scoop: in Australia’s credit reporting system, your score is influenced by your credit history (loans, credit cards, repayment behaviour, etc.), credit inquiries, and the types of credit you have. Having a mortgage and paying it on time is generally positive for your credit history, as it demonstrates you can handle a large loan responsibly. When you eventually pay it off and close the account, the loan will be marked as “paid” on your credit report – which is a good thing. This record typically stays on file for years (positive credit histories can remain for up to 2 years for repayment history, and the account closure for longer), indicating you successfully repaid a loan.

In the short term, it’s possible your score might dip slightly when you close a longstanding account. This is because you’d have one less credit line in the mix. The slight dip can also happen simply because of changes in the total credit available vs used, etc., not because the bureaus think being debt-free is bad (they don’t!).

Important: Your score would be negatively impacted if you missed payments or defaulted – but we’re talking about early, full repayment here. Assuming you’ve kept up all payments, an early payoff won’t show any negative marks. In fact, clearing your mortgage improves your overall debt-to-income ratio. It means you have more free cash flow – factors that future lenders will consider favourably, even if the credit score number itself doesn’t skyrocket.

Overall, don’t let fear of a credit score drop dissuade you from clearing your mortgage.

3. Tax Implications of Early Mortgage Payoff

- For owner-occupiers in Australia, there are no tax deductions on mortgage interest. This means from a tax perspective, you’re not getting any benefit from the interest you pay, and conversely, you won’t lose any tax benefit by paying the loan off early. In countries like the U.S., people speak of losing the mortgage interest deduction if they pay it off early. But in Australia, the interest is purely an expense. Paying it off as fast as possible generally makes sense since you’re eliminating an after-tax cost. There’s also no tax on imputed rent or anything – once you own the home outright, you essentially “earn” the benefit of living there rent-free, and that’s not taxed. In addition, any capital gain when you eventually sell your primary residence is usually tax-free and a good reason to pay off your mortgage completely.

- For investment properties, the considerations differ. Interest on an investment loan is tax-deductible against your rental income and possibly against other income under Australia’s negative gearing rules if the rent doesn’t cover the interest. Some investors purposely don’t pay off their investment mortgages quickly because they prefer to direct money elsewhere while the tenant and tax deductions cover much of the interest cost. If you have an investment property or think you might turn your current home into an investment in the future, think carefully before pouring all your spare cash into the loan. Paying off an investment loan early will reduce your interest deductions, meaning you’ll pay more tax on other income. Of course, you still save more in interest than the extra tax, but the net benefit is smaller. For instance, if your interest rate is 5% and you’re in the 37% tax bracket, each dollar of interest costs you 63 cents after tax (since the tax deduction effectively subsidises 37 cents). So paying an extra dollar off that loan saves you only 63 cents net. In contrast, paying a dollar off your non-deductible home loan saves you the whole dollar in interest. Prioritise paying off non-deductible debt (your home) over deductible debt (investment loans).

If you want to keep your first home as a future rental, use an offset account instead of directly paying down the loan principal. Why? Because if you later move out and rent the place, the interest on the remaining loan becomes deductible. Any money you had put into offset can be pulled out to purchase your next home’s deposit, and the original loan amount and its interest stays high – meaning a bigger tax deduction while the property generates rental income. On the other hand, if you had paid down the loan, you can’t re-borrow it for personal use and then claim that interest; the principal reduction is permanent. So, an offset in this scenario gives flexibility: you achieve the same interest savings while you live there (so you pay faster in effect) but preserve tax efficiency if it becomes an investment later. This is a niche consideration but valuable for younger buyers who might upgrade homes and convert the first one to a rental.

- Consider Capital Gains Tax (CGT) if you are directing money to investment vs home. Paying off your home doesn’t directly relate to CGT since your principal residence is exempt. But if you were investing extra money in, say, shares or an investment property instead, any gains from those might incur CGT when sold. Superannuation investments are taxed at 15% on earnings and potentially 0% in the retirement phase. It’s worth factoring in these differences when deciding where each extra dollar goes.

- Superannuation: Putting extra money into your super either via salary sacrifice or personal contributions has tax advantages. Only 15% tax on contributions up to certain limits, which is lower than most people’s income tax rate. Over decades, compounding in super can be powerful. But money in super is locked until retirement. Many young homeowners opt to focus on the mortgage now (which gives a more immediate, guaranteed benefit of a paid-off home), and plan to ramp up super contributions once the mortgage is gone. Others do both concurrently. Just remember it’s somewhat comparing apples and oranges: one secures your home ownership and the other boosts retirement funds. Both are important.

In summary, for your own home, there’s no tax downside to paying it off early – you’re not missing out on any deduction. For investments, weigh the value of deductions and consult an accountant if unsure. If your financial plan includes investing, whether in super or other assets versus mortgage payoff, consider the after-tax returns of each option. It can be worth getting personal financial advice to strike the best balance for your situation.

Case Study: Paid Off Mortgage Completely in 10 Years While Raising a Family

Sarah, a mother from Brisbane, provides a more down-to-earth example. She and her family paid off their home loan in 9 years and 8 months. Here’s a glimpse of how they achieved it:

- Set the goal early: Even before buying, Sarah and her husband had a goal to pay off the home in 10 years. This mindset helped them make decisions – from how much house to buy, to how frugally to live. They treated the goal as non-negotiable, which is powerful. It kept them motivated, especially when others were sceptical or when progress seemed slow.

- Consistent extra payments: They made extra payments whenever possible and stuck to a budget that prioritised the mortgage. Sarah mentions celebrating when they made the final payment and reflecting on how every time they found spare money, it went to the loan. They certainly experienced setbacks such as car breakdowns. But they hung in there, continued with their plan, and caught up.

- Lifestyle adjustments: During the payoff period, they kept expenses in check. They cut unnecessary subscriptions, bargain hunted, and didn’t inflate their lifestyle as income grew. They went on camping trips and picnics rather than expensive outings. Once the mortgage was gone, they could start doing more fun stuff – booking a three-month caravan trip in NZ, for example – which was a long-held dream they postponed. This highlights a common thread in early payoffs: temporary sacrifice for long-term reward.

Sarah’s case is relatable because she didn’t necessarily have an outrageous income or unique situation – it was good planning, persistence, and teamwork with her spouse.

Government and Banking Regulations

The journey to paying off your mortgage doesn’t happen in a vacuum – broader government and banking policies shape the environment for borrowers. Australian first-home buyers should be aware of certain regulations, schemes, and economic factors that can influence your mortgage and how you manage it:

1. ASIC and Responsible Lending

The Australian Securities & Investments Commission (ASIC) is the regulator that oversees consumer credit and financial advice. ASIC has published guidance (like the MoneySmart website) encouraging borrowers to pay down debt and use features like offset accounts or extra repayments wisely. In fact, the MoneySmart service we cited earlier is an ASIC initiative and provides free calculators and tips to help Australians get ahead on loans. In terms of regulations, Australia’s responsible lending laws require banks to ensure loans are suitable and that borrowers can afford them. This indirectly helps you pay off your loan because it prevents banks from lending you far more than you can handle. Lenders typically assess your ability to pay even if rates rose, so you should have some buffer.

While responsible lending obligations have been eased for certain loans, banks still follow guidelines to not overstretch borrowers. As a first-home buyer, you probably noticed the paperwork and questions about your expenses – that’s part of this framework. The idea is to avoid situations where you can’t even consider extra repayments because you’re struggling with the basics. If you feel overcommitted despite passing the bank’s checks, take a hard look at your budget. Regulators provide avenues if you’re in hardship, but ideally, you plan well so you can proactively pay extra rather than reactively seek help.

2. APRA Guidelines and Lending Environment

The Australian Prudential Regulation Authority (APRA) is the banking regulator that ensures banks, credit unions, etc., are safe and stable. APRA doesn’t deal with consumers directly, but its rules on banks greatly affect home loan availability and terms. For instance, APRA sets capital requirements, which has led banks in recent years to charge higher interest rates for investor loans and interest-only loans because they are deemed riskier.

APRA also introduced a rule that banks must use a serviceability buffer – currently at least 3.0% above the loan’s interest rate – when assessing new mortgages. So if you got a loan at 5%, the bank checked you could afford payments at 8%. This buffer is there to protect you and the system if rates rise (which they have) or if you want to pay extra. This means that if you can afford that higher assessed payment, you might have room in your budget to pay off your mortgage faster.

Remember that buffer when setting your repayment goals – just because the bank approved a certain loan doesn’t mean you should borrow to your absolute max if you intend to pay it off fast. Many prudent first-home buyers borrow a bit less than the max or maintain their own buffer. High household debt is seen as a vulnerability to the economy, so there’s an underlying push to keep it in check. By proactively reducing your personal debt, you’re also improving your resilience to any economic shocks – something APRA would silently give a thumbs-up to.

3. First-Home Buyer Schemes and Support

The government (federal and state) has several first-home buyer schemes that, while mostly focused on helping you buy a home, can indirectly affect your mortgage repayment strategy:

- First Home Owner Grant (FHOG): Most states provide a one-time grant of $10,00 or more to first-home buyers purchasing a new property or, in some states, any property under a certain value. If you received a FHOG and put it into your home purchase, your loan is effectively smaller than it would be. This jump-starts your equity and means less debt to pay off. Use that head-start wisely – continue to act as if you didn’t get that free $10k by paying extra, and you’ll pay off your mortgage completely in a shorter time. The grant itself doesn’t require any special repayment. It’s free money as long as you meet living requirements, but be mindful of conditions, such as if you need to live in the home for a minimum period to keep the grant. Otherwise, you might have to pay it back, which could set you back on your mortgage plan.

- First Home Guarantee (formerly First Home Loan Deposit Scheme): This federal scheme allows eligible first-home buyers to purchase with as little as a 5% deposit without paying Lenders Mortgage Insurance (LMI). Essentially, the government (through NHFIC) guarantees the lender the difference up to 20% deposit. If you buy using this scheme, you likely have a 95% LVR loan. Your priority should be to chip away at that principal aggressively to build equity (reducing the risk of falling into negative equity if property values fluctuate) and eventually getting below 80% LVR. There’s no requirement to pay it down faster under the scheme, but since you didn’t have to pay LMI, putting what you would have spent on LMI into extra repayments could be a smart move. Note: if you do refinance out of the scheme before reaching 80% LVR, you might have to pay LMI then, as the guarantee won’t transfer.

- Family Home Guarantee: A similar scheme for single parents allowed buying with just a 2% deposit. If you use this, you have a 98% LVR (!) loan. All the above advice goes double – try to pay it down to a safer level as soon as you reasonably can. The government guarantee has your back to 80% LVR, but any extra equity you can create gives you and your family more security.

- First Home Super Saver (FHSS) Scheme: This scheme lets first-home buyers make voluntary contributions to their super (up to $50k total can be withdrawn) to save for a deposit faster by taking advantage of lower tax on super contributions. If you used FHSS, you essentially treated extra savings as an investment, then pulled it out to buy the house. After purchase, you might wonder: should I now contribute extra to super or extra to my mortgage? This circles back to the opportunity cost discussion. The FHSS got you a deposit, but going forward, direct spare money where it yields the best outcome. Many first-home owners, after purchase, temporarily pause extra super contributions to focus on the mortgage since housing debt is now the larger concern. Remember to revisit your super strategy once the mortgage is under control or paid off so you don’t shortchange your retirement.

- Stamp Duty Concessions: In many states, first-home buyers get full or partial waivers on stamp duty for properties under certain values. For example, in NSW and VIC, homes under a threshold mean you pay no stamp duty. This can save tens of thousands. If you benefited from this, that money could be funnelled towards your mortgage principal instead. Think of it like this: you had budgeted X for purchase costs but didn’t have to pay that duty – if possible, apply a chunk of that “saved” cost into an initial lump-sum loan payment or set it aside in offset. It’s a great way to pay off your mortgage completely.

- “Help to Buy” and other shared equity schemes: The federal government has proposed a Help to Buy scheme (not yet fully rolled out as of early 2025) where the government would co-buy up to 30-40% of the property with you, reducing your loan needs. Some states like WA and VIC have their own shared equity programs, too. If you are in such a scheme, paying off your mortgage early is a bit more complex – because you might also consider “buying out” the government’s share down the track. These schemes typically let you purchase additional equity from the government as your savings allow. If your goal is to own 100% of your home, you’ll be juggling between paying off your part of the mortgage and accumulating funds to increase your share. Make sure to understand the rules – sometimes, the government’s share doesn’t incur interest like a loan, but they take a proportional share of capital growth. From a pure debt perspective, you only have to pay your mortgage portion, but psychologically, you might aim to also eliminate the co-owner. This is a unique case where buying more of your house is akin to paying off a mortgage. Definitely get financial advice because the optimal strategy might be to first pay off your part entirely, then save to buy out the rest, or vice versa.

In short, leverage government schemes to your advantage. They’re designed to ease the purchase, but the faster you can stand on your own (no guarantees, no shared equity, etc.), the better. Always meet any conditions of the schemes to avoid penalties that could derail your plans.

4. Economic Factors and Interest Rate Trends

Your plan to slay the mortgage will inevitably be affected by the broader economy – especially interest rate movements. Like the rest of the world, Australia saw historically low interest rates in 2020–2021 as the RBA’s cash rate dropped to 0.10%, and some mortgage rates fell below 2%. Then, in 2022, inflation surged, and the RBA began aggressively hiking rates. Right now, the cash rate is around 4.10%, and average variable mortgage rates have climbed to multi-year highs (around 6%+ for many borrowers). This whipsaw in rates has a few implications for you if you want to pay off your mortgage faster:

- When interest rates rise: More of your repayment goes towards interest and less to the principal, slowing down your progress. It can also squeeze your budget, making extra payments harder to find. However, in such times it’s even more important to try to maintain your repayment level or increase it if possible, because otherwise the loan term will extend. If rates jump, consider at least paying the difference to keep your original payoff timeline. Rising rates also mean new extra payments are more valuable – each dollar you pay off saves you higher interest.

- When interest rates fall: You get a golden opportunity to accelerate progress. If your required repayment drops due to a lower rate, keep paying the old amount. You were already used to it, so you won’t feel a difference, but now, every payment packs a bigger punch on the principal. Many Australians took advantage of the low rates in 2020/21 to pay down debt faster or build big buffers in offset/redraw. In fact, by 2022, over 70% of Aussie borrowers were ahead on their mortgages (with sizable redraw/offset balances), which has helped them cope with the subsequent rate rises. If rates fall again in the future, plan to do the same.

- Economic cycles and job security: Always be mindful that paying off a mortgage early is a marathon, possibly over a decade or more. In that time, the economy can go through ups and downs. Recessions, pandemics, booms – each can affect your employment or income. Build flexibility into your plan. For example, when times are good (the job is secure, maybe bonuses or raises are coming), try to make larger extra payments. When times are uncertain, you might temporarily hold extra funds in an offset or savings until you’re confident, rather than committing all cash to the loan. Having funds accessible, even if technically “earmarked” for the mortgage, can be wise if you fear a layoff.

- Inflation: High inflation can be a double-edged sword. It often causes higher interest rates, which is bad for mortgages, but it also means future dollars are “cheaper” in real terms. If your wage grows with inflation, your mortgage payment might feel easier over time. Historically, many people found the later years of a 30-year mortgage much easier than the early years because their income was much higher while the payment was fixed. However, relying on inflation to erode your debt burden is risky – especially if interest rates keep stepping up with inflation. You don’t want to pay double the interest cost just hoping your salary inflates. It is better to actively pay down and not depend on macroeconomics to rescue you.

- Household debt levels: As mentioned, Aussie households carry a lot of debt. This means the RBA is very aware that rate changes have big effects on consumer spending as more income goes to mortgages. There’s speculation that the “new normal” for interest rates might be lower than decades past, simply because people have such large loans now that even moderate rates pinch hard. But again, that’s speculation – plan for a reasonable range of scenarios. A good practice is to test your budget at, say, 2-3% higher than your current rate (just like the bank’s buffer test). If you can still make extra payments under that scenario, you’re in a safe zone. If you’re barely keeping up at current rates, caution is warranted – you may need to adjust spending or temporarily pause extra payments to build more emergency funds.

In summary, stay informed. Watch the RBA announcements (they meet monthly except January to review the cash rate). Understand that when it comes to interest rates, what goes up can also come down – and vice versa. Economic factors will influence the speed of your mortgage payoff journey, but with the strategies we’ve discussed, you remain in the driver’s seat to reach the destination.

Common Mistakes To Avoid

In the excitement of wanting to pay off your mortgage completely ASAP, it’s easy to fall into some traps. You should watch out for these common mistakes when implementing mortgage payoff strategies:

- Overcommitting Your Finances: It’s great to be enthusiastic about extra repayments, but don’t throw every dollar at your home loan without keeping a safety net. One big mistake is neglecting to budget for irregular expenses such as car repairs, medical bills, etc., or not having an emergency fund because you dumped all spare cash into the mortgage. If an unexpected expense pops up and you’ve got no savings, you might end up putting it on a credit card or needing to redraw from your loan therefore losing progress). To avoid this, establish an emergency buffer of 3–6 months’ worth of living expenses before aggressively overpaying your mortgage.

- Ignoring Other Financial Goals/Investments: As discussed, focusing solely on the mortgage while ignoring other opportunities can be a mistake. For example, if your employer offers matching super contributions, that’s essentially free money for your retirement. So don’t opt out of that just to have a few extra dollars for the mortgage you’d be missing. Likewise, if you have absolutely no investments, pouring all wealth into your home means you’re not diversified. Your house will grow in value, but it’s a single asset. The mistake would be having a fully paid-off home at 45 but nothing in super or investments and then having to play catch-up for retirement. Avoid the “asset-rich, cash-poor” scenario where all your money is locked in the house, and you have nothing liquid for opportunities or needs.

- Misusing Redraw or Offset Funds: Having redraw and offset facilities gives flexibility – but that can be a double-edged sword if you’re not disciplined. One common pitfall is treating your home loan redraw like an ATM. For instance, you make extra repayments faithfully, but then you see a nice chunk available in redraw and decide to splurge on a holiday or a new car using those funds. Essentially, you’re undoing your good work (and adding interest cost back). Only dip into redraw for genuine needs or opportunities, not wants. The mistake is a lack of self-control with these tools. If you fear you’ll spend it, maybe a stricter loan with no easy redraw would ironically be better for you. With offset, another misuse is not depositing all your income there. To maximise offset benefits, you ideally route your salary and all deposits into it and pay expenses from it so that every day your loan interest is offset as much as possible. If you instead keep money sitting in a regular account earning near-zero interest, you’re not fully utilising the offset and are effectively paying more interest than you need to.

- Neglecting Insurance Protection: When you have a large debt, especially if you have a family, insurance is vital. We’re talking life insurance, total and permanent disability, income protection, and even trauma cover – the kinds of insurance that pay out if you die, become disabled, or can’t work due to illness/injury. It may not seem directly related to mortgage payoff, but it absolutely is. If something tragic happened to you or your partner and you couldn’t work, how would the mortgage be paid? The mistake is focusing on killing the debt, but not shielding against worst-case scenarios.. Many super funds include a default level of life and disability cover – check if it’s enough to cover your mortgage and support your family. If not, consider topping it up or getting a separate policy. Having the right insurance means you won’t wipe out years of hard-earned progress or force a distress sale of the property if life throws a curveball.

- Not Having a Clear Budget and Plan: Some people just say “I’ll pay extra when I have spare money”.Without a plan, it’s easy for that spare money to vanish into lifestyle creep. Avoid the mistake of winging it. Instead, create a budget that includes a line for extra mortgage payments, just like a bill. Automate it. Track your progress – maybe use a spreadsheet or an app to see the balance decline and estimate your mortgage-free date. This keeps you motivated and on course. Having a plan doesn’t mean it’s inflexible – review it annually. But it gives you a roadmap. Those without a plan often fall into another mistake: using extra cash for short-term desires.

- Failing to Seek Advice When Needed: Lastly, don’t do it alone if you’re unsure of something significant. For instance, if you’re considering refinancing or complex offset setups, talk to a mortgage broker who can lay out options. If deciding between invest vs pay off, a session with a financial planner could illuminate what’s best given your goals. Experts can spot mistakes you might overlook – like the tax implications of paying off an investment loan, the insurance gap you might have, etc. The cost of bad decisions or missed opportunities often exceeds the cost of advice. Even reading reputable personal finance resources like ASIC’s MoneySmart or books by financial experts can help you avoid missteps.

In summary, stay balanced and informed. Yes, be aggressive in paying off your mortgage completely, but not to the point of recklessness. Avoiding these mistakes will ensure that your journey to mortgage freedom is smooth and that you don’t sabotage your own efforts.

Frequently Asked Questions (FAQs)

When applying for a home loan, lenders will ask for your recent bank statements to verify your income and expenses. Typically, Australian lenders require about 3 months of bank statements for your everyday transaction account and savings account.

This is a classic dilemma with no one-size-fits-all answer. It boils down to your financial situation, goals, and risk tolerance. Paying off your mortgage brings a guaranteed return and emotional relief of being debt-free. Investing, on the other hand, offers the potential for higher returns but comes with risk and no guarantees. A sensible approach for many is to do both: ensure you're meeting your mortgage obligations and making some extra payments, while also contributing to investments

Making extra repayments is one of the best things you can do. The immediate effect is that the extra amount goes straight towards reducing your principal balance, which in turn reduces the interest charged. Unlike a regular payment (which covers interest first, then principal), a pure extra payment isn't eaten up by accumulated interest – you've already covered interest with your normal payment. The result is your loan will finish sooner than the scheduled term and you will pay less total interest over the life of the loan

In many cases, yes – especially in an environment where interest rates or your loan situation has changed since you got it. Refinancing means switching your loan to a new lender or negotiating a new deal with your existing lender)to get a better interest rate or terms. It can absolutely be worth it because even a seemingly small rate drop can save a lot. By refinancing, you become a "new" customer to someone and get that sharp rate. However, consider a few things: If you're already well on track to pay off your loan very soon, refinancing might not yield huge benefits (since interest cost is naturally declining)

Yes, if you have a redraw facility on your home loan, you can pull out (redraw) the extra repayments you've made, subject to your lender's rules. Think of redraw as a loan feature that lets you borrow back some of what you prepaid. This can be a lifesaver in emergencies. However, if you want to pay off your mortgage completely, then don't touch your redraw except for true emergencies. A discount on a holiday to Italy is not an emergency!

Final Thoughts

Paying off your mortgage completely is a marathon, not a sprint – but as we’ve shown, with the right strategies, mindset, and awareness of potential pitfalls, you can significantly shorten that marathon. Many Australians in their 20s, 30s, and 40s have done what seemed impossible: killed a 30-year mortgage in a fraction of the time. By making smart financial moves, leveraging features like offsets and extra payments, staying informed on interest rates and regulations, and keeping balance in your financial life, you, too, can join the ranks of happy homeowners who truly own their homes outright. The journey may require sacrifices and careful planning, but the reward – full ownership and the financial freedom that comes with it – is absolutely worth it.

Next Steps And Paying Off Your Home Loan

Our team at Hunter Galloway is here to help you buy a home in Australia. Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Start again

Start again