In a recent address, RBA Governor Philip Lowe shed light on the distressing consequences of increasing interest rates for Australian homeowners. This article delves into the tough choices faced by the Reserve Bank and their effects on mortgage repayments. We will also explore the latest updates and unexpected twists in the housing market, covering topics such as skyrocketing prices, regional recoveries, and the potential implications for buyers and sellers.

To learn more, read on or check out the video below.

Table of Contents

The Challenge Faced by the Reserve Bank

Governor Philip Lowe acknowledged the significant impact of the bank’s actions on individuals with home loans, especially recent buyers burdened with hefty mortgages. He emphasized the necessity of using interest rates to maintain a supply-demand balance and mitigate inflation. While recognizing the unequal distribution of effects, Lowe stressed the importance of utilizing available tools.

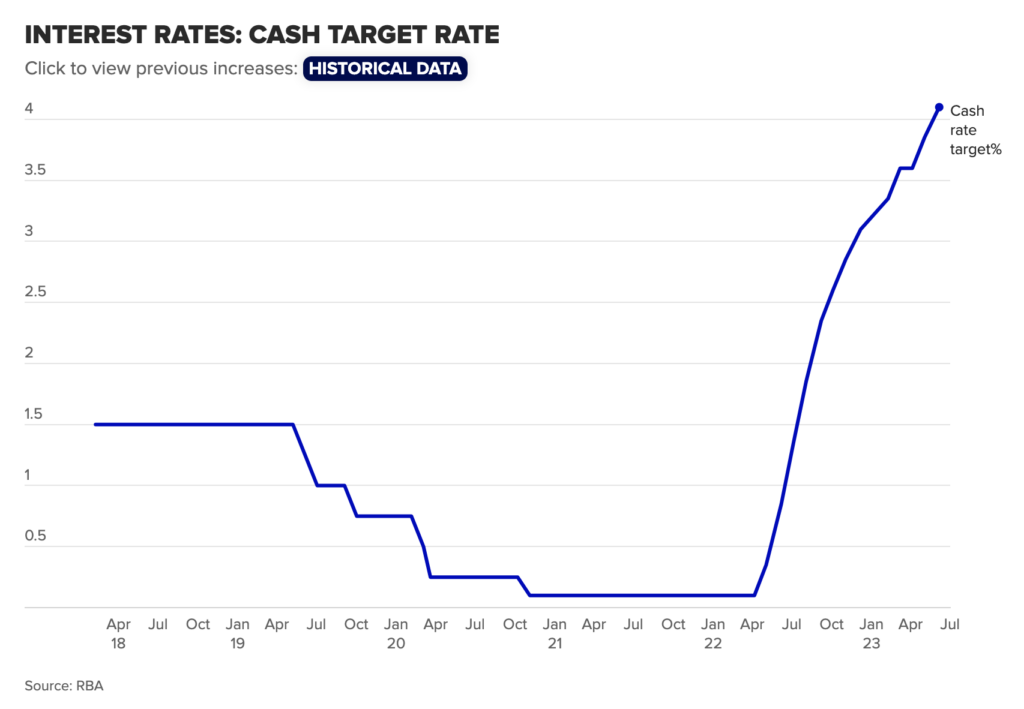

The RBA's Decision

To combat inflation, the Reserve Bank recently raised the interest rate to 4.1 percent. Governor Lowe explained that while some households may face short-term financial strain due to increased mortgage rates, not raising interest rates sufficiently would lead to greater medium-term costs. Failing to address inflation could result in an extended period of elevated living costs, necessitating even higher interest rates later on.

Balancing Inflation and Economic Stability

Governor Lowe acknowledged the challenges of reducing inflation without causing a recession or a drastic rise in unemployment. High interest rates, wage increases, and sluggish productivity growth pose additional hurdles in bringing inflation down to the target range of 2-3 percent. Boosting productivity growth becomes crucial to mitigate inflationary pressures from wage increases.

Housing Market Updates

Beyond rising interest rates, it’s important to consider the latest developments in the housing market. The Home Value Index (HVI) by CoreLogic revealed a third consecutive rise, with a 1.2% growth in May 2023. Sydney stood out, experiencing a 1.8% increase in home value, its highest monthly leap since September 2021. Brisbane and Perth also showed positive growth.

Recovery in Regional Areas

Regional areas displayed signs of recovery, albeit slower than capital cities. The combined regional index grew by 0.5% in May, reflecting an upward trend. However, the growth rate of regional homes lagged behind that of the capitals. Tight housing supply and declining internal migration rates contributed to the disparity between capital and regional markets.

Challenges and Uncertainties

Potential rate hikes may increase mortgage stress and lower consumer sentiment. Rapidly growing housing prices could lead to inflation risks through the “wealth effect.” Refinancing fixed-rate home loans could escalate mortgage stress. However, demand from net overseas migration is expected to persist, partially offsetting these factors.

Conclusion

As interest rates rise, the impact on Australian homeowners becomes increasingly apparent. The Reserve Bank faces the challenge of balancing inflation and economic stability, making tough decisions affecting mortgage repayments. Understanding these complexities and staying informed about housing market updates is crucial for homeowners, buyers, and sellers alike.

Start again

Start again