Refinancing your home loan is a smart financial move that could save you money over the long term. If you have a home loan, you are probably getting bombarded right now by your next-door neighbour and even the 7 o’clock news – all talking about refinancing.

So is now a good time to refinance?

There are a few different situations where refinancing could make sense for you. In this article, we’ll explore some key reasons you may want to refinance your home loan in 2025.

Let’s dive in…

Table of Contents

What is refinancing?

Refinancing means changing your existing loan for a new one and, in most cases, with a new bank. In other words, Refinancing a home loan involves replacing an existing mortgage with a new one that has different terms.

The two main reasons people look to refinance their home loans are:

- to get a better rate or

- to increase their existing loan to withdraw some home equity.

You can refinance your home loan from any bank or lender you choose; you don’t have to stick with your existing lender. These days banks do not reward loyalty. In most cases, we find lenders offer better deals to new customers rather than rewarding their existing ones.

Aside from this, what are some other reasons for refinancing? It will come down to your personal situation and short to medium-term goals. While people have many reasons for refinancing, here are the most common ones we see.

1. I want to reduce my home loan repayments.

| Loan amount | $ 350,000.00 | $ 400,000.00 | $ 450,000.00 | $ 500,000.00 |

| 3.75% | $1,620.90 | $1,852.46 | $2,084.02 | $2,315.58 |

| 4.00% | $1,670.95 | $1,909.66 | $2,148.37 | $2,387.08 |

| 4.25% | $1,721.79 | $1,967.76 | $2,213.73 | $2,459.70 |

| 4.50% | $1,773.40 | $2,026.74 | $2,280.08 | $2,533.43 |

| 4.75% | $1,825.77 | $2,086.59 | $2,347.41 | $2,608.24 |

| 5.00% | $1,878.88 | $2,147.29 | $2,415.70 | $2,684.11 |

The craziest part is the power of compounding interest.

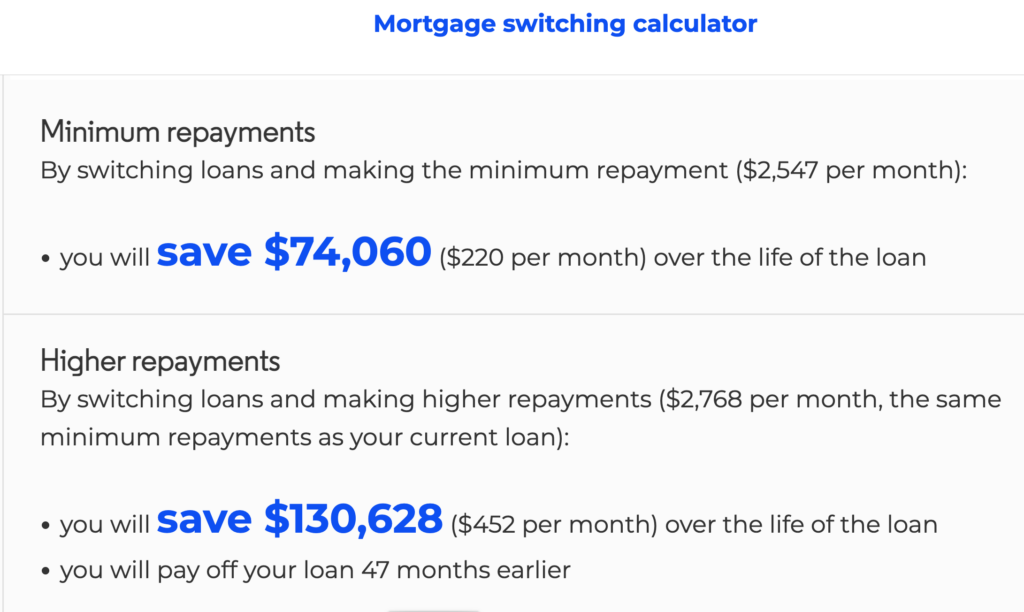

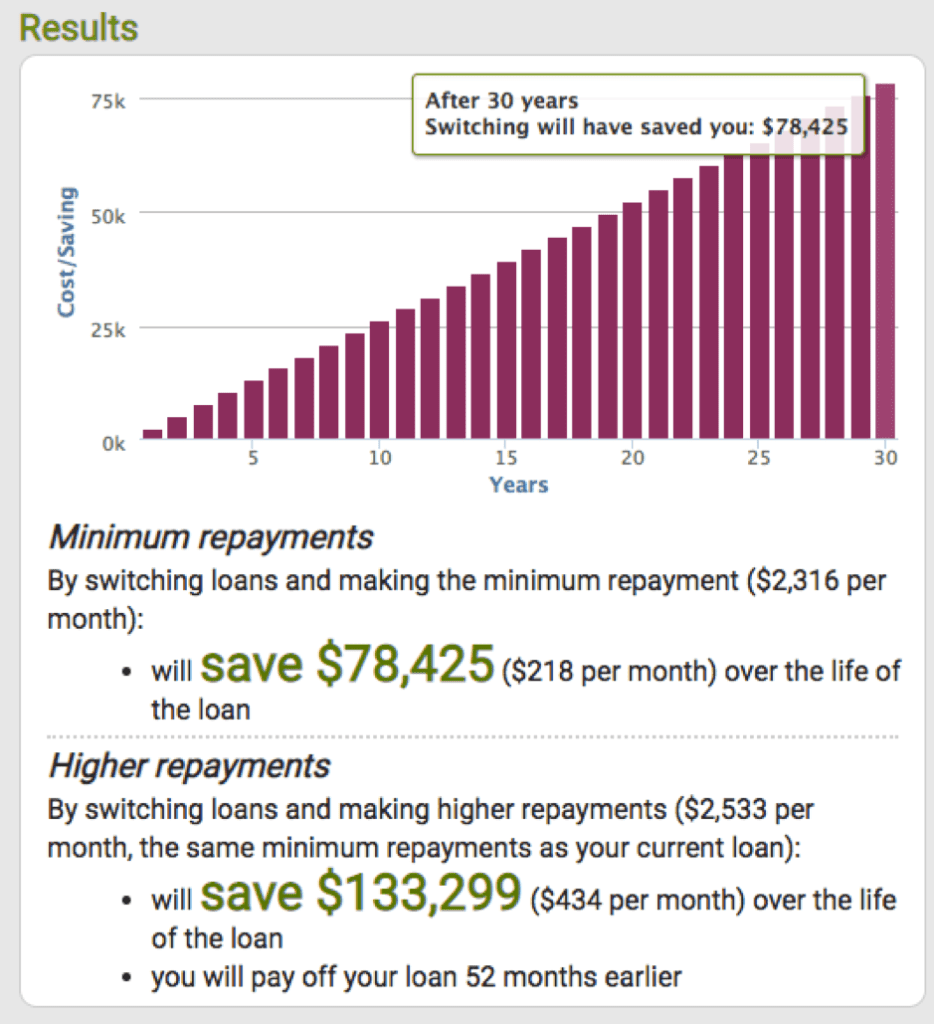

Using the ASIC MoneySmart refinance calculator to do the numbers, if you were to switch to the new lender with an interest rate that is 0.75% lower on your mortgage of $500,000, you would not only save $220 per month, but you would save $130,628 over the life of the loan!

2. My property has increased in value.

If your property’s value has gotten a boost, you might be able to refinance and get a better rate. These days banks give better interest rates to borrowers with more equity.

For example, if you bought your home for $500,000 and had a loan of $450,000, but the property’s value has since increased to $600,000, you have increased your home equity from 10% to 25%, and lenders will be more willing to give you larger discounts to get your business. This will reduce your interest costs and help you repay your loan faster!

3. The fixed rate period on my loan is expiring.

It is very common in Australia to have a fixed rate term of between 1 to 5 years. When your fixed rate finishes (or expires in bank talk) at the end of that 1-5 year period, your loan will change back to a variable rate.

In most cases, the bank’s standard variable rate will not have any discounts! You can avoid this higher interest rate by switching to another fixed rate or even refinancing to another lender.

4. I can afford to pay more off my loan.

For some people, changing the length of your loan term can help pay off your loan quicker. If, for example, you have had an increase in income and can now afford higher monthly home loan payments, you could refinance to a shorter loan term. In this case, you could reduce your loan term from 30 years to 25 years, helping you pay your home loan off faster and saving you literally tens of thousands of dollars in interest payments over the life of the loan.

Let’s go back to the example above. Say you had the home loan of $500,000, and you refinanced your loan to a new interest rate of 3.75%. If you were to keep the repayments the same as what you paid with your old bank at $2,535 per month while on the lower interest rate, you would save $133,229 over the life of the loan and pay off your home loan 52 months earlier. In other words, you would slash 4.3 years from your home loan term!

5. I want to increase my loan and take cash out.

A cash-out refinance allows you to use the equity you have in your home to borrow money at a lower cost. You may want to invest these funds into shares or use them as a deposit for a new investment property.

How exactly does increasing your loan work? Let’s say your house today is worth $600,000, and you have $450,000 left on your current mortgage. This means you have $150,000 in home equity. You could refinance the home loan to withdraw $30,000 of this equity into a home loan, bringing your total lending to $480,000.

You can potentially borrow above an 80% LVR (loan to value ratio), but you would need to pay for lenders mortgage insurance, so it would be best to talk to your mortgage broker and understand what these numbers look like.

6. I want to do some renovations.

After you’ve been in your home for a few years, you might feel it’s time to do some renovations. These generally fall under 2 categories:

- Simple renovations, like adding air-conditioning, solar panels or painting. If you are doing a simple renovation, the numbers work exactly the same as taking cash out, and you would rely on the equity in your home.

- Structural renovations, like adding an extra level to the house, a pool or a new kitchen. With Structural Renovations, you can rely on the on- completion value of the renovated property.

So, for example, if you are adding an extra bedroom and bathroom to the property, which would increase the home’s value by an additional $100,000 – the bank can lend on this figure. Using the example above, if adding an extra bathroom and bedroom increases the property’s value from $600,000 to $700,000, you could then increase the lending to $560,000, meaning additional lending of $110,000, which can go towards your renovations.

7. I want to consolidate other loans (and credit cards)

Lastly, you can refinance to consolidate other loans and debts into a single and possibly more affordable payment. This can be handy in situations where you have high-interest-rate loans and debts like credit cards, personal loans or car loans.

A debt consolidation home loan refinance works similarly to a cash-out refinance, where an increased portion of the loan can be used to pay out other loans and debts. Your old home loan would increase by the amount you used to pay off those other debts.

Debt consolidation works well if you have lots of different credit cards and are paying really high interest rates. The only downside when consolidating debts is to consider the new loan term and what the total interest costs will be after you have consolidated everything.

Bonus: Pros and cons of refinancing your mortgage in a falling housing market.

The Australian housing market has seen a downturn, with interest rates reaching historical highs and reduced borrowing power, causing house prices to decrease. This has left many homeowners concerned about their financial security, and many are considering refinancing their home loans.

But with the decline in property values, the question arises: is it the right time to refinance?

Generally, the refinancing decision for each individual is unique and depends on your personal goals and needs. We have covered some of the reasons you can choose to refinance your home loan.

But it’s important to weigh the pros and cons before deciding to refinance in a falling housing market.

Pros:

- A lower interest rate refinancing may be a solution to reducing the interest and monthly repayments. We’ve seen 9 consecutive rate rises, which have led to interest rates hitting some record highs. This has led to higher repayments and mortgage stress for many. Refinancing to a lower rate might alleviate some of the financial strain caused by the current interest rate environment.

- If you’re willing to pay a higher monthly payment, you can refinance to a lender that offers the option to reduce the overall term on your mortgage. This can lead to paying off your home loan sooner, so you won’t have to worry about rate rises anymore. It’s important to note that this option requires you to pay a higher monthly repayment, and it’s good to check with the lender if you’re refinancing to a variable option with a lower interest rate to ensure they allow additional repayments or lump sums to be paid.

- As we mentioned earlier, we have already had 9 consecutive rate rises. If you are worried about more rate rises, you can switch to a fixed rate and secure your monthly repayments by refinancing to a fixed interest rate. This can provide stability in the face of potential rate increases. Fixed-rate home loans keep your payments consistent for a set period regardless of changes in the market. So, although your home value may be decreasing, you can still protect yourself from potential future risks by choosing a fixed-rate home loan.

Cons:

- Less Equity. Many homeowners are worried as the decrease in the value of their homes has led to a drop in the equity available. This drop in equity can impact the rates offered by lenders and even the likelihood of your loan being approved.

- Falling into negative equity. Negative equity is when your home value has dropped below the outstanding amount you owe to the bank. In this situation, you won’t be able to refinance your loan because, technically, you’re lending 100% of the property value. In many cases, when you refinance, the lender wants to lend at an 80% LVR with no mortgage insurance or a maximum of 90% LVR if you’re paying lenders mortgage insurance. If you fall into negative equity, you may not have any other option except to stay with your current lender, increase your monthly repayment and wait until the property price increases again.

- Lower borrowing power. As rates have risen, this lowers your borrowing power, which makes it even harder to qualify for a home loan. We are seeing this quite a lot. You may be making all of your repayments, but when you try to refinance, lenders may say that you can’t afford the loan you already have. This is because the banks add a buffer of about 3% above the current rates when they assess your application. In effect, they are looking at your ability to repay a mortgage at, say, 8% instead of the current rates, which are about 5%. In other words, if rates have gone up since you’ve borrowed, you might actually not qualify for a loan now because of this assessment.

- Potential for additional costs. When your property value drops, the percentage of it you need to borrow to refinance goes up, which can be quite costly. Effectively as soon as you’re lending over 80% of the property value, things like lenders mortgage insurance become applicable. You may still be able to refinance your home loan, but typically lenders require a 20% equity to avoid that lender’s mortgage insurance. There are some lenders that will waive the mortgage insurance up to an 85% lend, but they can charge higher interest rates.

Bonus: Cost of refinancing a home loan in Australia.

While there are heaps of benefits to refinancing your loan, you must remember there are still costs to complete the loan application. You may have to pay some of the following costs when refinancing your home loan

- Break Cost. If you are on a fixed rate and decide to refinance it to a variable rate or to move to another lender, your current lender may charge you break costs (also known as break fees).

- Discharge settlement fee. This is also known as a loan exit, settlement, or termination fee. Some lenders make you pay this fee in order to cover administration costs when you exit a loan.

- Application fee. In some cases, you may need to pay an application fee. Some banks may waive this fee to get your business. So, talk to your mortgage broker to see if you can get this fee waived.

- Property valuation fee. Sometimes if you are refinancing to a new lender, they may require a property valuation. This also differs from lender to lender.

- Settlement fee. Some lenders may charge this fee, especially if there are legal costs involved.

- Mortgage registration fee. You may have to pay some government fees when you change your mortgage.

Generally, these costs can range from $400 to $600 for a single property refinance.

But the good news is that many banks offer refinance rebates at the moment, and in some cases, we have been able to arrange up to $2,000 refunded to our refinance clients on settlement to cover the costs of switching and also leave them with some change! There are some terms and conditions to the refinance rebate, so chat with our team at Hunter Galloway to see if you qualify.

Next steps and refinancing your home loan

We’re more than happy to help you walk through your refinance options and find the right option for you. You can schedule a call with one of our Expert Mortgage Brokers or get started with your refinance journey here.

Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Start again

Start again